The Fed at this point controls the whole economy and they have two options:

1. Raise interest rates and stop printing. Crazy inflation stops, but asset prices crash and we enter a major recession or depression. The end result will likely be unrest and blood in the streets.

2. Do nothing, keep printing. Inflation picks up massively. The economy keeps humming along but young people, including myself, are permanently priced out of home ownership and many other things. We enter a new era of cyberfeudalism, which probably involves some blood in the streets.

It seems like they are going with option 2. I am 24 years old and I can't say I'm particularly excited. It doesn't even really seem like any of the high paying jobs are enough to keep up with this insane market. All I can do at this point is raise my fist to the sky and say fuck the fed, fuck the financial system, fuck the greedy rich, fuck BlackRock, and fuck you.

This is only part of the problem - and a small part of the problem at that.

The real problem as always is zoning. Houses cost roughly the same on a $/sqft basis, adjusted for inflation, as they did in the 1970s. They're more expensive now because outside of town they're twice as big on average [1] - in part due to zoning rules. In town, zoning rules preclude densification necessary for supply to meet demand [2]. And, families are smaller.

Check out Japan housing CPI - a market where supply meets demand thanks to federal zoning rules, and is also centrally banked. Dead ass flat. [3] This chart alone basically debunks the theory the Fed is solely responsible for lower housing affordability.

Zoning is the issue, not the Fed.

[edit] Yes, the fed contributes a little - monthly affordability of a more expensive house is the same when interest rates are lower, but down payments are not. However, if you want to solve the affordability crisis build more houses. Any houses. Now. Compare the Japan housing CPI in [3] to the US housing CPI in [4] and weep. Housing in the US is driving inflation, not responding to it.

While I agree zoning is a huge issue (I think that interest rates being so low doesn't help, either, but I concur with your thesis that zoning is the bigger problem), this, however:

> Houses cost roughly the same on a $/sqft basis, adjusted for inflation, as they did in the 1970s.

Sorry, but no. My parents bought their first home for $72/sq ft. real¹. They sold it for $99/sq ft. The same house last sold for $208 sq ft., and is Zestimated today at $302/sq ft. The value of the home has averaged >7% gains YoY, well outpacing published inflation.

Their current home, built significantly later, and like you say, significantly larger, was $149/sq ft. at purchase, and is $182/sq ft. today.

Every house I look at sings this same tune. Accounting for inflation, where my parents got a large house ready to move into, for the same amount to day I'm looking at what I call a "contractor's paradise", and that will require significantly more than the sticker price to make it habitable.

¹all dollar figures in this comment will be in 2021 real dollars, not nominal ones. I.e., adjusted for inflation.

The inflation adjusted $/sqft statement is a blended average across the US. It’s lower outside of towns and higher inside towns. This is tracked by the Census bureau but as always with averages there are values on both sides of the mean. [1]

One caveat is it does reflect only new construction.

You're conflating the market for suburban family homes with the market for real estate. What about apartments, commercial real estate, etc.? Rent has absolutely exploded, which might not be priced into suburban family homes that aren't built to be rented and don't directly compete with more urban apartments.

under market, no. but due to locality there are a lot of different real estate markets. dragging prices of wyoming into the dataset when you are interested in nyc or sf makes just no sense. then you have the problem of the different types of new constructions too. i don't see how averaging helps here.

at least where i am looking (european country), cities have roughly seen a 100% price increase since 2010. income hasn't kept up with inflation or the housing prices.

Part of the problem with the first item you mentioned is that developers don’t really want to build cheap housing (I guess this is an assumption, but it makes sense financially.) They can make way more money catering to the people who can “afford” to build a $500k home, and people who want a very custom design and lots of space. On the renting end, “luxury” apartments will make more money than really basic cheap units. So most of the new housing stock doesn’t help address the problem for people new to housing. Even if you want to build out a very basic, small house, you have to have cash to DIY without a bank, or find some way to finance a builder (increasing the significant labor cost) without having existing equity. So the part of the market that does want cheap, basic housing doesn’t even have a way to influence those units. There is loads of demand for them (young people without money make up a huge portion of the population), but no developers willing to meet that demand when they can just make expensive units. And not enough developers so that some need to chase the cheap market.

And in cities, the lot cost is very prohibitive too, before even getting into building a very basic house.

> Part of the problem with the first item you mentioned is that developers don’t really want to build cheap housing (I guess this is an assumption, but it makes sense financially.)

This is like saying that Toyota would rather sell Lexuses than Camrys.

Yes, it's true, but they sell Camrys anyway. Why? Because the market for luxury is only so big. They can make more money total addressing other parts of the market.

So why doesn't this apply to housing? Land + zoning. Imagine if Toyota was only allowed to produce 10,000 cars a year. What kind of models would they choose to make?

Can only speak for my city (Seattle), but no one’s building Camrys and building is constant. It’s not because any zoning prevents building affordable units. It’s because there’s limited land to develop at all and demand for property of any kind is extraordinarily high. All of the development in residential neighborhoods is already zoned for everything that could accommodate 4-10 times as many tenants. But they’re building luxury units anyway.

Doesn’t surprise me but this zoning explanation ain’t it.

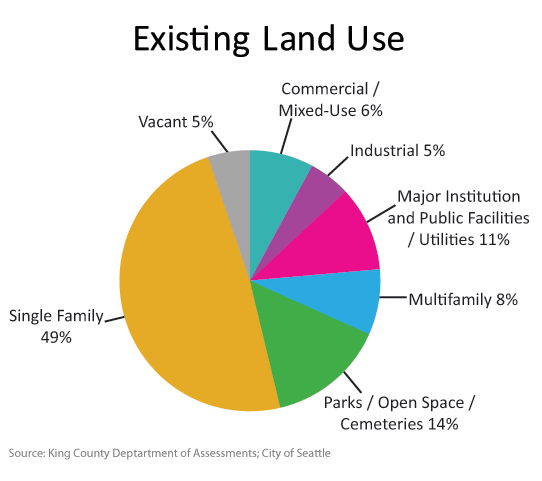

50% of the developable land in Seattle is designated for single-family homes, and not one single inhabitable SFH in Seattle city limits is what anyone would call "affordable". The fact that it's illegal to replace those SFHs with duplexes, quadplexes, or midrises is a primary driver of housing unaffordability.

Seattle's population growth has outpaced its housing growth for multiple decades. There's a huge amount of "catching up" to do, and SFH zoning is blocking that from happening.

Once enough there's enough housing to hold all the rich people that want to live here, of which there are many, you will see some downmarket construction happening. But we're a long way away from that.

They’re replacing SFHs with multiplexes all over the city all the time. Instead of assigning A/B/C units or fractions they just split the numbers already designated for the lot.

Zoning for MFHs won’t change that. It’ll maybe bring more skepticism to luxury developments. But people buying million dollar units with no lot will know they’re buying the same thing.

And mixed use luxury apartments are the only development otherwise. No one is building anything more affordable in zoning more favorable for it. At best this is trickle down economics where everyone who needs somewhere affordable to live might be able to get scraps at the most dangerous furthest flung place in Lake City.

So if this is a "problem" for government to fix via either Zoning being abused or the free-market being naughty, then why doesn't the government just create very specific and targeted "high-density, high-rise, cheap-price" zone that can only be built with the right and necessary units?

Dude have you been to lake city? The only area that’s dangerous is where there city built one street up with all projects. It’s significant safer than Ballard university district and and capital hill

> As of 2019, there were 367,806 housing units in Seattle, representing a 19 percent increase since 2010 (according to Washington State Office of Financial Management). The growth in the number of housing units in Seattle from 2010 to 2019 surpassed the 14 percent growth seen between 2000 and 2010. However, even with the rapid increase this decade, expansion of our housing stock has not kept up with Seattle's population growth of 22 percent between 2010 and 2019.

And here's Seattle's land zoning ("Land Use" tab on the same website):

> Can only speak for my city (Seattle), but no one’s building Camrys and building is constant

I'm in the Seattle metro. Building higher density housing is still illegal in most of the city, because attitudes there are still fundamentally NIMBY, even if it's not as bad as SF.

The city has generally upzoned little slices at a time around 'urban villages', and while that's certainly better than nothing, it's a lot less effective than largest scale upzones, and streamlining building processes.

This is a poor analogy. People rely on cars way differently then they rely on housing. If the only car you could buy was a Lexus, you might stretch you budged, take out a big loan and buy one, or you might simply not buy a car, get a bicycle instead, take the train, a cab, or pay a coworker to carpool.

Housing doesn’t give you this option. If you don’t want to be homeless you may be able to rent, but that is pretty expensive too.

It seems to me like your list has analogs in housing without squinting too hard: spend more of your budget on housing, get a mortgage (big loan and buy one), get a smaller place (bicycle), rent a place (train), or move in with roommates (carpool).

So many landlords have taken old homes and converted them into single apartments, raising the cost without creating any value. I would say destroying something of intangible value as well. That trend has definitely driven the cost of housing up.

Because selling a Camry doesn't reduce the selling price of Lexuses built in proximity to it by more, in aggregate, than the profit from the Camry. Which is why developer-founded and controlled HOAs have much more restrictive rules than public zoning rules.

One theory, and this may just apply to my location, starter homes supply is being eaten up by firms who are going to turn around and rent it out. So they are essentially grab what little supply there is of new construction starter homes, then turning around and renting them out for quiet a bit of a sum that still prices quiet people out of them unless they are fine eating shit.

We don't seem to have an issue with Hertz coming in and scoping up all the camrys.

There are plenty of yuppies to buy up any fancy new houses in town, though. So no cheap houses are built inside the cities proper.

In the US, there's always more land - it's just further away! The cheap "Camry" houses still get built, but never as infill. It just gets pushed further and further out to the exurbs.

Unless you take money (or cheap debt) out of the hands of the yuppies, nothing changes here.

It doesn't really matter if you add new stock at the top end or at the bottom end, people from the bottom move up, and make space at the bottom for new entrants. Any new stock you add increases supply, which leads to lower prices across the board.

[edit] and btw, I think builders aren't tripping over their shoelaces to service the low end of the market because they know the city is so aggressively capping how much they can build. This means they will only build the most profitable units, the high end today. But once the high end is saturated, the low end ones will be the profitable ones anyways.

> It doesn't really matter if you add new stock at the top end or at the bottom end, people from the bottom move up, and make space at the bottom for new entrants.

Only if the old housing stock isn't torn down to make room for the new housing stock. Thankfully property taxes aren't driven in the potential value of land (rather, they are tied to actual value), but most small scale landlords of affordable housing right in it are in it for property appreciation, not rents. Their exit plans are often to sell to a developer as tear downs.

> This means they will only build the most profitable units, the high end today.

There are costs are too high (to acquire property and build) to justify anything but going after the highest end of the market. Once the high end is say satisfied, money (investment) could simply move away from housing if it can't make any money there. Money chases the highest returns between all of the markets, not just one market.

> Thankfully property taxes aren't driven in the potential value of land (rather, they are tied to actual value)

That's not a thankful thing at all, it incentivises using the limited land in wasteful (low-value) ways.

> Once the high end is say satisfied, money (investment) could simply move away from housing if it can't make any money there. Money chases the highest returns between all of the markets, not just one market.

Available capital is practically unlimited these days, anything that's profitable and legal to build will get built.

> Only if the old housing stock isn't torn down to make room for the new housing stock

This is about zoning too. Normally, if the demand is there for it a smart land owner would build more housing on the same plot, e.g. turning a single family into a two family, but of course that is illegal in many places.

Yes, that is exactly what is happening in Ballard (Seattle area) right now. Those cheap 100 year old low income housing complexes (one or two stories) are being raised for a bunch fo three story townhomes, smart developers can sell each of those town homes for $1 million each, and they could get much less if they kept it as a hotel-like complex. I just bought one of those town homes, so I'm not going to complain too much, but I'm self aware about what is going on here.

So poor people are still getting screwed. My daily walk to the grocery store passes by a few places that are pretty shabby (so low income) and right across the street they are building a bunch of luxury town homes. It doesn't take a rocket scientist to figure out what will happen to those shabby places in a year or so.

> a smart land owner would build more housing on the same plot

This is an uncomfortably extremist position, should maximizing revenue per investment be the one and only consideration society takes into account?

I do many things that provide joy in life in other ways, even if I know they don't maximize revenue or savings. I wouldn't want to go through life thinking about nothing else than ROI for every action.

>property taxes aren't driven in the potential value of land (rather, they are tied to actual value)

That means multifamily properties have higher tax bills for absolutely no reason. Expensive locations need to provide more housing per area so charging a fixed fee based on the value of the land is a much better approach. You get to build a single family home and pay through the nose or split the bill with a multi family home.

I hear this repeated a lot. In practice, at least in the cities I've lived in, I've only seen housing go downmarket when there's an explicit exodus. The reason is that housing is built for a specific living space size. Los Angeles has so many single family houses that it's impossible to cater to people downmarket...unless houses are torn down and multi-unit housing is built. You could rip those down and build upscale, large apartments, but I feel like I see them sitting vacant instead of moving downmarket. The bust sucks for everyone and the boom (gentrification) sucks for the less well off.

Maybe we're saying the same thing, but instead of gradually reaching a equilibrium like you're describing I see a dramatic boom bust cycle--both are held back by lack of building.

> It doesn't really matter if you add new stock at the top end or at the bottom end, people from the bottom move up, and make space at the bottom for new entrants. Any new stock you add increases supply, which leads to lower prices across the board

I could definitely see that being how it works in a lot of cases, but it seems like a stretch to assume that's some sort of natural law of prices. If I have a market of ten potential buyers, the first who has $1, the second who has $2, and so forth until the tenth buyer has $10, I could put an infinite number of goods for $10 for sale, and none beyond the first would be able to be purchased. Sure, you could argue that it would be silly of me to price in that way, and you would be right, but in reality you don't know the exact financial details of every potential buyer of your whole market. GP is hypothesizing that basically this exact scenario is happening with housing, and I don't know if they're right or not, but your rebuttal doesn't seem very convincing that this is an impossibility.

My point is that it's at least mathematically possible for a scenario to exist where the assertion I was responding true does not happen. If the idea is that _in practice_ people always lower the prices, then it seems more direct to just say that rather than claim some sort of law of economics that doesn't actually have any mathematical proof.

If they priced at $6, they’d sell 5 units for $30 and 5 people would still be unable to afford to buy housing while the seller held onto 5 more units waiting for another person to come along with $6. If they priced at $7, they’d sell 4 units for $28, which still might be better for them.

This might not be that far off from what’s happening.

We have the same problem with the car market. I can only afford a $5,000 car, but the car manufacturers make all their money building $20,000 cars. I just can't see how Honda making another $20,000 fit is going to help me afford a $5,000 car.

The problem from the manufacturers' perspective is that the gear required to meet 2021 safety, emissions, and fleet efficiency standards by itself almost pushes a new car's price over $5000, and that's without leaving any budget left over to make it a car anybody would want to buy.

They do sell vehicles at that price which get around all of those standards, but they lose two wheels in the process.

You used to be able to buy a decent used car for $5k but as of recent you can't find any without connections. I've been telling folks interested in Japanese cars that it's $10k at this time to buy used with low mileage for a sedan and $15k to buy used with low mileage for an SUV.

I mean VW makes $100,000 Porsches and $20,000 Jettas. At some point it’s not economical to make cheaper cars due to materials and workmanship. You can certainly buy an e-bike for half that, I did.

The cost of construction in America is $150/sqft. We’re not even close in cities. Off by an order of magnitude.

Sorry I guess I was more obtuse than I intended. My point was I can buy a used car for $5,000, and Honda building new cars allows that even if the new cars are out of my price range.

Some analysts believe that in another 5-10 years in the US, you'll get if not quite a $5K USD car off the Internet, a $10K USD car from a Chinese manufacturer, and the Detroit automakers will reprise their arrogance-into-bankruptcy role from the 70's again when Japanese cars entered the US market, when they famously remarked the new entrants can have that cheap unit market.

Watching the Detroit product roadmaps, I'm inclined to agree with that analysis at this time.

In cities with no zoning todays luxury housing is tomorrows affordable housing. For example in Houston apartments and houses that were touted as luxury in the 80s are slums now.

This also holds for smaller cities in the Rust Belt. My childhood home, purchased almost new in 1980, is only worth about 2x what my parents paid at a time of 20% interest rates. It has been very well kept and sits on about an acre and a half. Everyone with means has moved away. Retirees and people with no better options are all that's left.

We're seeing a massive demographic shift to single person households all across the first world countries from Canada to Korea. But for some reason the housing market is still geared towards families.

Households with two or more incomes are more likely to be able to afford real estate than single-income households - both in absolute income levels as well as in economic crisis where it is less likely all family is losing their all of their income simultaneously than a single person..

If the real problem was always zoning, wouldn't dense cities like NYC and Shanghai be cheaper than average, not way over average?

> Check out Japan housing CPI - a market where supply meets demand thanks to federal zoning rules, and is also centrally banked.

Japan went through a huge bubble in the 1980s. Also, housing (the structures at least) rapidly depreciates in Japan, which prevents them from being used a speculative asset as in countries (even then they still went through a huge bubble in the 80s). It is definitely an alternative model to our own, but I'm not sure how many people will want to experiment with that. Japan also much more strictly restricts immigration than other countries, which makes it, for example, a bad place for Wenzhou house wife real estate speculation.

> If the real problem was always zoning, wouldn't dense cities like NYC and Shanghai be cheaper than average, not way over average?

It's not about supply by itself, it's supply vs demand.

Big cities have big populations and economies, which means a lot of demand.

But as far as zoning goes, note that like other metros, NYC has actually effectively downzoned areas over time; in fact, a huge proportion of buildings there would now be illegal due to different types of density restrictions: https://www.nytimes.com/interactive/2016/05/19/upshot/forty-...

A lot of NIMBY's tend to go, "well, there's still some areas where it's possible to build more, so there's no real issue there". This is approximately like restricting car manufacturing to one state, and then when car prices go through the roof, saying "well, there's still more land to build car factories there, so I don't see the problem, it couldn't possibly be this rule".

NYC housing has pushed outwards into Queens and the Bronx, manhattan is less populated these days because it lacks full time residents (the apartments are still sold, but their owners list upstate/Connecticut/long island properties as their permanent addresses, and they have many less occupants in them even when full, not like the turn of the century when more than a few people were crammed into small apartments).

> A lot of NIMBY's tend to go, "well, there's still some areas where it's possible to build more, so there's no real issue there". This is approximately like restricting car manufacturing to one state, and then when car prices go through the roof, saying "well, there's still more land to build car factories there, so I don't see the problem, it couldn't possibly be this rule".

My only point was that making cities more dense seems to make them more desirable, causing more people to want to live there. Yes density is a great thing! But it doesn't solve affordability problems on its own. Can you imagine if San Francisco (6.2k/sqm) had NYC-level density (27k/sqm), would it be more or less affordable? I'm going to go with the less.

What is really holding us back are the American libertarians who are afraid of a public housing system like the one in Singapore.

> My only point was that making cities more dense seems to make them more desirable, causing more people to want to live there.

Increasing housing in this manner would probably boost land prices, but over a greater number of units, so result in overall decrease in housing cost.

NYC is a bit of a weird spot in real estate, in that having a Manhattan address (and probably a Williamsburg or Bushwick address to a lesser degree these days) is a status symbol for foreigners, in the same way that London or Paris might be. Most American cities do not have this kind of cachet and so at some point prices will fall if you build enough.

The problem is really that housing production would have to increase by an incredible amount to get to affordable. To use the example of Tokyo as affordable, let's look at comparative housing production statistics.

* The 23 special wards of Tokyo, 8.9M people, built 110,000 new homes that year.

* The entire country of England, population 53M, built 115,000 homes a year.

* The metropolitan area of NY, population 20.3M, approved 27,000 units in 2012, but approvals != actual construction.

> * The 23 special wards of Tokyo, 8.9M people, built 110,000 new homes that year.

Since housing is refreshed in Japan on a 20-30 year basis, you can't quote the number of housing built without comparing it to the number of housing torn down (since, as mentioned before, housing depreciates).

> * The metropolitan area of NY, population 20.3M, approved 27,000 units in 2012, but approvals != actual construction.

So the way it works in NY IIRC, you can get an approval and not actually act on it, and the reason you can do this is because the approval can be sold with the property, which isn't an uncommon thing.

NYC does not track construction starts like that, or at least not when that article was written

Demand isn't unlimited, and you have the causation mostly backwards. Cities being successful causes people to flock to them, which means there's demand for density.

The problem is that it isn't just those on the right opposed to density -- the left is little better. Sure, progressives are largely okay with what density already exists, but propose upzoning and they flip out. Just look at the California state legislature, or major west coast cities.

Demand is pseudo unlimited. The real problem is betting on a single location. All 300 million Americans won't fit into new york. Why not build more new yorks?

New York became a hub for commerce and culture because it was a very successful port city. With the completion of the Erie canal, it connected the American heartland to the Atlantic Ocean. This naturally led to it being the main port for immigration as large numbers of people came to the US in search of economic opportunity. Decades of sitting at the center of the northeast corridor, the richest metropolitan area in human history, has made it a solid contender for the financial capital of the world. You can't simply build more New Yorks, the geography and history that produced it are unique.

Of course not everyone wants to live in New York, indeed there are many cities that each have their own unique circumstances drawing vast numbers of people, and all of them experience great demand. But there's a reason you can't just through up a bunch of skyscrapers in South Dakota and get everyone to move there.

> My only point was that making cities more dense seems to make them more desirable

You have it backwards, it is making the spot desirable that leads to them becoming dense. More people keep moving in, you build denser to accommodate them. Can you imagine how expensive NYC would become if 77% of current residences suddenly stopped being unavailable?

Yes, you will have some non-linear effects, people do want to live in big cities where the action is, but the reason those cities exist in the first place is because the action's already there. New York is a massive hub of commerce and culture which is ultimately a consequence of it's position as a major port. You won't make it undesirable by decreasing density so long as its still the center of the financial world.

I'm pretty sure this is wrong. Yes, it's the first answer that comes up if you Google this stat, but this is off by a factor of 3 or so. Before the pandemic San Francisco had a density of around 18K/sqm. Although a lot of people left SF during the pandemic, 6.2k/sqm is still way to low.

Now, that we have that out of the way. In general, I agree with you. Most cities that have a high population density are expensive places to live. It's a good thing to allow cities to accommodate more people, but those places will still have a high cost of living, because many people still want to live there.

Doesn't it make sense though? In 1910, manhattan was expensive but a lot of people still lived/worked there. The apartments would be crazily subdivided so you could fit 10 people into a 3 or even 2 bedroom. Now they are all owned by wallstreet bankers with small families, and they spend much of their time somewhere else (they might not even list their manhattan apartment as their "main domicile" during the census).

Demand for Manhattan apartments is crazy high, it's just illegal for taller ones to be built to meet demand most of the time.

People think Manhattan is mostly skyscrapers, but the reality is very different. Only a small portion of the land has high rises on it, just glance at Google Maps with 3D view on.

Manhattan is mostly multi level apartment buildings, at least 4 stories or so. I don't know why your point would contradict mine. Yes, units in the taller skyscrapers are more expensive and sell for tens of millions of dollars, if not more.

I wonder how NYC would do with cheap 30 story Chinese concrete apartment blocks? (30 stories, because any taller requires steel, at least with construction practices that use cheap migrant labor).

This pattern of living is still common to a lesser degree in outer-borough immigrant neighborhoods, which is why they were so hard hit during NYC's massive COVID wave.

No, demand is actually down in Japan[0]. That chart shows residential housing vs. under 65 year-old population. So demand is decreasing but residential RE is rising slightly. Your analysis is also ignoring that services cost a lot more in the US than they did in the past. You can't build cheaply in NYC or SF or Seattle anymore because construction workers cost more.

The idea that zoning is the issue is always funny to me because it’s very easy to disprove. Plenty of paces in the US have permissive zoning (like the NY metro area). If zoning was the issue, then one would expect affordable housing in these areas, but it is still totally out of reach for most.

> Zoning issues/lack of supply would imply that there are lots of homeless people without a roof over their head.

The price of housing only matters to people who don't already have homes they own. 65% of Americans own homes, so that cuts down your working set dramatically.

There are a lot of homeless people, yes - 0.2% of the population - but lack of affordable housing tends to be roughly equivalent to "perma-renting" as renting has a lower barrier to entry.

To buy a home you have to come up with a lump sum of money to make a down payment. If you can't do that, you're forced to rent or split accommodation or live with your parents. Lack of affordable housing doesn't mean homelessness. There's a lot of elasticity there.

> Investors have too much access to property. It's a system of greed that benefits those who entered the market early (typically boomers).

Investors buy property to rent because home ownership is unaffordable. Blackrock buying up property is a symptom of the market, not a cause. They don't see houses becoming cheaper because they don't see zoning reform on the horizon, so they believe there will be long-standing demand for their rental units.

If housing were to become affordable, due to a large increase in supply, these investors would get bowled over twice - once due to lower real property value and once more due to lack of demand for rental units as folks buy instead.

Even foreigners parking capital abroad, more supply makes that (a) a bad idea and (b) kind of irrelevant. I'm not saying that shouldn't be tackled too, but once again, zoning would solve the problem.

There are lots of homeless people. There's an even larger population of people who are, for example, living in their parents basements, or over-occupying small apartments, or commuting for hours because they are living in distant, cheaper areas.

The die was cast for option 2 30 years ago. Once policy flipped to “we will provide capital to prevent bad things”.

Half the economy is based on real estate… people building buildings to avoid taxation (if you have $) and borrowing against equity (joe homeowner). You cannot break equity values without breaking the economy.

The people who are getting screwed are the same people who have been getting screwed since the Vietnam era. Go watch “clerks” and read early 90s op/ed pieces - it’s the same cycle.

A lot of large corporations are basically real estate companies. You know, companies like McDonalds.

It's actually funny how the efficient market hypothesis makes no sense once you consider the role that land has played in human history. It's the biggest unsolved problem in economics that no politician really acknowledges.

Even anti government or extreme free market ideologues still insisted that land should be heavily taxed or regulated in the name of efficiency.

In retrospect, it rings true. I think I had my eyes opened during 2008 crisis and FED was effectively buying everything thrown at it. I remember thinking how can government own its own bonds?

> I think I had my eyes opened during 2008 crisis and FED was effectively buying everything thrown at it.

They definitely did not. [1]

The bailouts were largely loans, ones that were repaid to the US government for a pretty substantial profit, not less. And assets the Fed took on were literally that, assets, which the Fed was profitably unwinding before COVID hit.

On the chart shown at your link, Fed-owned assets go from ~.8T to 2.5T (blue line, assuming the MBS (red line) are part of that.) and then grow as QE takes effect and the Fed buys all manner of things. That .8T was all US Treasuries, no longer true of the expanded balance sheet. If you look at the updated chart (https://fred.stlouisfed.org/series/WSHOSHO), whatever you make of it, it doesn't look like much in the way of loans getting repaid. Whatever you want to say about loans being repaid, I think that the 1.5T (conservative number) that the Fed spent buying non-UST assets was then spent by the sellers on raising other asset prices not on paying down loans.

The bailouts were via Treasury. [1] QE was via the Fed. I believe, and correct me if I'm wrong, back in 2008 the Fed could only pick up bonds and maybe mortgage backed securities?

You can see the Fed unwinding its balance sheet here [2], up until 2020, and in the link you provided.

If the Treasury lends out ~700B for ~MBS and is repaid ~700B for MBS, and the Fed buys $1-2T (low end of the repayment you mention) in MBS, who is really doing the bailout?

Treasury made loans with repayment schedules to specific businesses. The Fed purchased certain kinds of assets to hold temporarily on their balance sheet.

They both filled different roles - one was meant to manage inflation and the other to secure the stability and function of the markets. The Fed's dual mandate is to maintain maximum employment and low, predictable inflation rates over medium term. Spotting Ford in a rough patch doesn't fit the mandate.

It seems to me that tripling the monetary base and investing two parts of it in MBS is going to have an inflationary effect on house prices. Am I being obtuse here?

To be clear, I don't think you're being obtuse at all.

Fractional reserve lending means that an increase in the monetary base is a result of lower interest rates - money supply operates on a pull model not a push model. Lower interest rates mean a more expensive house costs the same per month when mortgaged, which in turn increased the outstanding supply and balance of mortgages, hence new money. Lower interest rates increase the price of houses, but to a much lower extent the affordability of those houses - which is more likely to be measured on the monthly cost of a 30 year fixed loan. It will move the goalposts on down payments, however, but down payments are only 2-20% of the cost of the house.

In my opinion, however, I believe zoning to be a much bigger contributor to overall affordability.

So, I’m 36, and I promise you don’t want a deep recession. Cheap housing doesn’t matter if you don’t have a job. We dodged a freaking bullet economically with COVID. We recovered quickly. Heck, even in 2008 we did better than the countries that tried fiscal or monetary austerity.

And yeah, the real enemy is zoning. It’s fun to blame Blackrock, and they deserve it, but it’s regular homeowners trying to restrict more housing that is the cause.

I think graduating into the 2008 mess gives us peculiar point of view. Two years older, we might have already had burgeoning careers. Two years younger, we might have avoided it altogether.

I remember so much impending doom from those years. Pretty different than the current sentiment.

2002 here got into the market right after the 2000 bubble and the second Irak war… my lessons learned since has been to travel and go where the market is better.

Didn't mean to imply that things were back to normal by 2010, only that it was (in theory) possible to prepare for it a little. In my case, there's no way I would have dropped CS in favor of anthropology if I knew what my prospects would look like!

But yeah, it was rough for everyone. Even now, young careers are shaped by what happened in 2008.

One of the ironic twists is that EU is doing all the "hardcore" free market austerity stuff (think Greece's imposed austerity or Germany's balanced budget) while the US is doing the Keynesian stuff (tax cuts, stimulus checks, infrastructure projects).

That's not true, the Netherlands has a budget deficit of 60 billion this year saving the economy from COVID. The US gives money directly to citizens while Northern European countries are giving it to businesses.

I am also 36 and zoning is not stopping me from buying a house, lack of trucking to move out of state is because I want my stuff to actually show up in a reasonable amount of time.

Inflation can be good for young people. If you really think there will be significant inflation, go buy a house, borrow more than you are comfortable with it necessary. Inflation will make the debt easier to deal with in time.

This is borderline romantic at this point. What bank do you think would ever possibly agree to this? Most people can’t even prove to their banks that they can afford a mortgage that’s less than the rent they’re currently paying.

There’s a lot more expenses as a homeowner than the mortgage (even the PITI (principal, interest, taxes, and insurance)).

I can’t think of a year where I didn’t have $5K of crap that needed fixing/replacement/improvements*, the year with the fence was 6x that, and I’ve got a boiler coming due that will be a $15K project in all likelihood, $25K if I go higher-end and improve the piping configuration for more even heat on the far end of the piping runs.

* not making improvements is a major saving point in favor of renting. Improvements are a money and time pit and most return less than $0.50 per $1.00 spent on them. It means you live without the improvement, but it’s wildly less expensive over time.

This sounds like someone buying 15yrs old heavily used car and complaining that all of the cars are expensive to upkeep.

Therefore its better to use taxis.

My mortgage cost are half the rent for same property I dont see myself loosing money anytime soon on my deal. Plus nobody will kick me out on the whim of truing rental into AirBNB like my parents got few months back.

> I can’t think of a year where I didn’t have $5K of crap that needed fixing/replacement/improvements

For a contrary anecdote, I've been living in my current house for well over 20 years and not once have I spent 5K in a year in maintenance. Rarely have I spent even over 1K.

I can't think how I could even spend that kind of money in maintenance every year. What's there to fix that costs you so much?

> I can’t think of a year where I didn’t have $5K of crap that needed fixing/replacement/improvements,...

To the younger generations out there mortgaging themselves into housing: the closer you are to median income, the more you should make damn sure you're computing PITI+Maintenance when crunching your numbers (there are a couple good calculators out there now, discussed in the past on HN), staying below a 33% post-tax DTI, and taking on as much of the fix/replace/improve work yourself as possible.

With increased US income precarity due to the medical debt adverse lottery selection pressure (major source of bankruptcy), conventional housing is a bigger gamble for median income earners, and conservative personal financial planning around housing mortgaging decisions is completely absent from mainstream American discourse. The field is entirely tilted against the common folk, and young generations in particular are specifically preyed upon.

With the high cost basis of housing today, try to avoid transaction churn and look to stay in one property for as long as the numbers make sense to you, and crunch the numbers for any moves to include round-trip realtor fees. At 2-3X gross pre-tax annual income for a house, while moving around and buying each time you move wasn't optimal, carrying the cost for big career income increases was justifiable. At today's ratios, with today's decreased class/income mobility, the round-trip realtor fees to sell-then-buy are tone-deaf by the industry to the reality on the ground for young customers.

The US real estate industry is tremendously out of alignment with serving the majority of the US population and especially the younger cohorts, and their extractive orientation only eats their seed corn to set up an asset bust down the road. The demographic time bomb that is now unfolding even in the US will be challenging to reverse/slow/halt, and has likely already indelibly written the secular asset bust into the real estate industry's future. No doubt the central bank will bail out the private underwriters again by making the quasi-public underwriting facilities take on the overleveraged valuations at their lows and unload as the private balance sheets can pick them up again to profit off them in the up cycle.

The real estate industry in general thrives upon a population who generally cannot get along with each other living in close quarters with each other as individuals, and that is also a hackable vector (among many others). If you can find extremely close (forged over 7-10 years) friends who you can thrive together even when living with each other under the same roof, then you've found a de-leveraging function against the industry's imposed costs instead of going at it yourself.

While all the efforts at YIMBY and related legislation are great, people need to get on with their lives and fund their retirements today. Hack your own solutions at your own level now instead of waiting for those efforts to bear fruit, because for damn sure the politician meat puppets of the real estate industry and the industry itself aren't ever going to do anything for us.

That's an ideological concern, not a financial one. The fact is that regular people can do very well investing in real estate, and inflation is very good for real estate investors.

Jerome Powell has already made it clear through his actions that everything is now 'Too Big To Fail'. Capital is at an all-time low in terms of actual real cost to the borrower.

You'd be an idiot not to borrow right now. If we keep seeing dramatic inflation, there will be some increase in wages, and it'll be enough to offset whatever interest rate you get, unless you're just an utterly unqualified borrower.

There's a reason /r/wallstreetbets exploded in popularity right around the time COVID-19 hit and money was being printed nonstop and assets were dramatically increasing in value... the hoi polloi know the playbook that the wealthy elite have been using, and now they're using it too.

There's no guarantee Jerome Powell will always be the fed chair (and if inflation really gets out of hand he could just be the fall guy).

But the bigger problem is that in an inflationary environment, real assets get bid up high to compensate. This has already happened in housing (clearly) so you're late to the party. If you knew for certain that inflation was going to get to this level before everyone else, maybe it would have been a good idea to do what you're describing.

> There's no reason to think you know what the future holds.

Prior behavior is the best predictor of future behavior. The world has become complacent and dependent upon cheap capital, and no one - and I mean no one - is ready or willing to turn off the faucet yet.

Prior behavior includes the 50% stock market crash in 2008 and ten year periods of negetive real stock market retutns. A financial plan that doesn't include a probabity of these events recurring isn't one I can get behind.

No expert recommends dwelling on only the most recent behavior.

Yes, but people were saying this several years ago too. The truth is no one knows what is happening. We're in a new market regime that has not been explored before. Everyone is just guessing what's going to happen. Some of them are going to be right and do very well. Some of them are going to be wrong. People will say the ones who were right were smart and the ones who were wrong were dumb.

As Adam Smith said, the true price of everything is in human labor. Inflation generally raises the cost/price of new labor at the expense of historic labor. Demand for labor is still high, the price will likely continue to increase.

Housing is also not a great comparison metric because it was so perturbed by 2008. New unit starts dropped precipitously and still have not fully recovered: https://fred.stlouisfed.org/series/HOUST

We know how to build housing quickly and now it's clear there is demand. If the current trend continues it looks like we will again have a housing surplus within the decade.

> As Adam Smith said, the true price of everything is in human labor.

Cite?

Also who died and made Adam Smith's word synonymous with fact?

Last I checked the true price of anything is the price I have to pay to acquire it, which is incidentally more in line with Adam Smith's actual quote which was: "The real price of everything, what everything really costs to the man who wants to acquire it, is the toil and trouble of acquiring it.". The price I have to pay to acquire something translates to money, that I gained through "toil and trouble" so to speak. Quite far from the true price of everything being human labour.

Wealth of nations, book 1, actually. "toil and trouble" could be interpreted as "labour". I certainly take that interpretation.

though Smith really didn't make much use of the labour theory of value, as he thought it would be less relevant in an advanced economy. Riccardo and especially Marx developed and used it much more. (For Marx see the first part of Capital)

> Wealth of nations, book 1, actually. "toil and trouble" could be interpreted as "labour". I certainly take that interpretation.

You are free to interpret it any way you like, but then taking your interpretation and saying that is what Adam smith was trying to say, when it is quite literally not what he said, nor even close to what he said, is called lying, and that is not really okay.

There's no need for interpretation, Smith makes it quite clear with nearly an entire chapter dedicated to it:

> The value of any commodity, therefore, to the person who possesses it, and who means not to use or consume it himself, but to exchange it for other commodities, is equal to the quantity of labour which it enables him to purchase or command. Labour therefore, is the real measure of the exchangeable value of all commodities.

> It was not by gold or by silver, but by labour, that all the wealth of the world was originally purchased; and its value, to those who possess it, and who want to exchange it for some new productions, is precisely equal to the quantity of labour which it can enable them to purchase or command.

> But though labour be the real measure of the exchangeable value of all commodities, it is not that by which their value is commonly estimated.

The idea of "value" independent of price is something treated by Marx as a normative claim that neither Adam Smith or Ricardo developed. When Ricardo or Adam smith talked of "value", they just meant "price" but in some notional unit of currency which was irrelevant to the discussion at hand. E.g. they wanted to discuss prices in a barter economy.

Adam Smith explored the labor theory of value in the context of primitive societies with fixed capital. In that case, you do get prices scaled to labor inputs, as capital is constant.

Ricardo tried to develop more sophisticated models than those with fixed capital, but did not have the tools to determine price setting, and finally admitted "I am not satisfied with the explanation I have given of the principles which regulate value.".

It wasn't until economists started using math more seriously and included production functions and utility functions that they were able to formulate a more general theory of price setting involving marginal costs and benefits. This allowed the creation of numerical estimates for things like price elasticity that provided useful information for price setting and allowed (in some cases) for falsifiability and even laboratory experimentation. See the famous experiments of Vernon Smith, for which he won a Nobel Prize. https://www.econlib.org/library/Enc/bios/SmithV.html

Thus standard economics was able to go bit beyond the thought experiments of Ricardo and Smith whereas Marx continued the process of philosophically musing about value in a normative sense, now removed from any actually observed prices, and far off into the world of political economy rather than economics per se.

Unfortunately none of the modern economic theories apply to real estate, because it is a land market in disguise and has little to do with housing.

Price of land is determined when looking at the world as a whole (margin of production), so it can't be measured in a simple microeconomic laboratory experiment.

It can actually be studied using models, but one would have to go back to Smith and Ricardo and add the third factor of production (land) back into the equation. Which was removed by marginalists for simplification to study simple markets of bananas and yogurts.

The modern economic foundations simply don't have the tools to study land markets, so they will always fall into the trap of a drunk man looking for keys under the lamppost only.

Honestly, I am disappointed with Marx. For every day people only two things really matter. Fix money (usury and debt) and land. Once you do that, there is no need for a communist utopia.

Is there any measures of what percent of those pre-2008 builds were speculative investments vs. occupant-owners? It reminds me of the scene in The Big Short when he knew the system was on a precipice of disaster when the a stripper was telling him about the multiple homes she owns.

It seems to me many bubbles are the result of speculation with easy credit and I’m not sure 2008 can be considered a “perturbation” instead of a correction.

Thank you. Maybe you can help me understand this correctly.

Your link shows the "owner-occupied" housing was relatively flat during the housing crises. The link below shows new housing units were still increasing during that time.[1] Does that imply most of the new builds were investment properties (i.e. not owner occupied) during this time period?

I think this is what matters most. It's good to have some vacancies so that people have options but too many likely indicates there's some speculation/over-building going on that the market doesn't support.

There's a world of difference between high interest rates (which are good and healthy) and rising interest rates (which implode the economy).

You gotta look at the derivative.

Rising interest rates are really, really bad. Anyone who relies on revolving business debt, credit card debt, or other non-fixed-rate debt goes bankrupt.

I kinda wish I entered the economy when we still had 12% interest rates. Each time a recession hits, we level it off by lowering them a bit, and we've kinda hit the floor.

I don't think we can get back to 12% interest within my lifetime without some kind of economic collapse or cataclysmic event.

> Anyone who relies on revolving business debt, credit card debt, or other non-fixed-rate debt goes bankrupt.

This is hyperbole. Rising interest rates aren't fun, but they aren't cataclysmic. Rates have gone up and down for decades. Further, if you signal that you're taking the option to raise rates off the table, risk tolerance and asset prices will explode (some would say this has already happened due to Fed signaling).

To explain more about the logic used by the guy you replied to...

...the problem is people think: interest rates go up, economy slows down, we can never raise interest rates. This logic takes on a life of its own.

The US economy was in this position in the late 60s: the Fed was under pressure to accommodate govt financing, they raised rates in 1959 and were blamed for causing a recession that influenced the outcome of the 1960 election, in 1967 they attempted to raise rates briefly but did so at the wrong time...eventual result (combined with some unfortunate timing with oil price changes) is rates never rise, inflation does, serious problems.

When the discussion moves to this point, and we have been moving this way for years, I think it is a sign that something has gone quite wrong. And that expectations around interest rates and Fed behaviour are actually adding volatility and uncertainty, not reducing it.

You are quite correct though. Rising interest rates are not bad. It is just the price of money. Falling interest rates can be just as bad too, but the problems are usually subtle (i.e. financial repression, which is what is happening now, no-one will realise what has happened until they try to retire in 20/30 years and realise they can't). Public policy has moved to this risky stage where people blame everything on politicians...the result is, unfortunately, inevitable.

This is the exact situation many financial commentators highlighted post-2008, so I think your historical points are very relevant.

The Federal Reserve is supposed to have independence from the government. It will develop its own monetary policy which doesn't need government approval. In reality, the President appoints all the Governors, so people get selected based on doing what the President wants done.

The Fed's monetary policy is typically an inflation target - keep the money supply growing to encourage growth, but keep inflation in check as well.

The problem is the political influence starts to impact the pure decisions about what's best for the economy. Election coming up? Well, hold off on increasing rates since we need good employment numbers for the next few months.

If the economy gets unstable the Fed ends up riding the razor's edge trying to stick to policy but not piss off the President. Problem is that the economy can go off the rails faster than the Fed can response.

The issue highlighted after 2008 was that "yeah, printing new dollars and buying distressed assets worked pretty well! and no massive inflation so far. But there will be incredible pressure to not raise rates later and if the Fed waits too long to apply the brakes, they won't be able to get ahead of it and inflation will skyrocket."

Chairman McChensey Martin (who served in the late 60s when all this started to blow up) used to say that the Fed is independent within government. So the Fed is able to develop policy independently but doesn't have room to actually run counter to whatever the Executive is doing.

I don't think the impact is necessarily elections anymore, if it ever was. But the Fed was supporting bond auctions through 2020. I don't think it will stop them raising rates but it has stopped them raising rates fast enough imo.

The apparently only empirical study relating interest rates and growth was done by Richard Werner, concluding growth actually historically happened in high interest rate environments, whereas the current economic dogma states exactly otherwise.

I don't know what his point is. There is no absolute level of low or high interest rates.

Interest rates merely balance the supply and demand of/for labor.

Growth usually happens when there is high demand for labor and that means interest rates are high during periods of growth. When you think about it, interest is just the risk adjusted yield of a labor saving investment plus minus bank fees and profit share of the borrower. That means the existence of high yielding investments is what drives interest rates up as lots of borrowers got to the bank and present their fantastic business ideas and the bank picks the highest yielding ones.

Well, I also have to say something. Growth didn't really stop with lower interest rates. The economy is much bigger than 30 years ago.

Also about negative interest rates, it's a fallacy to think they are supposed to stimulate borrowing. They are supposed to balance people's desire to be in debt with people's desire to hold onto credit (equivalent to demand/supply of labor). That means negative interest rates exist as a disincentive to save money because nobody wants to borrow money.

Richard Werner is a bit nutty but his work does have value. He takes a heavily heterodox position on interest rates, some of this is him being misleading in order to be controversial. But his points about the impact of interest rates on bank profits are very trenchant (and btw, the reason why he is a bit nutty is because his professional experience was Japan in the late 80s/90s, that scenario tested all the assumptions about macro and found a lot of them were false, his book Princes of the Yen is good...although, again, very heterodox).

The extent to which you might be right or wrong depends to some extent on how much debt there is in the system (or how leveraged/wound up the economy is).

A debt-based economy is much more vulnerable. Last time we raised interest rates rapidly, in the eighties, household debt was less than half of what it is today, adjusted for GDP.

Yes, whenever rates eventually rise, it's going to hurt some people. People and companies burdened with debt. Some will in fact go bankrupt (most will not, of course). But that's not a reason not to do it, all that is, is more evidence of fiscal irresponsibility. Any company which is unable to withstand higher debt costs is just as poorly managed as one which is unable to withstand a rise in any other input cost. If McDonald's went bankrupt tomorrow claiming rising beef costs, you'd say their business plan was flawed, being overly reliant on subsidized farming and not planning ahead for contingencies. The same is entirely true for a company that is bankrupted by higher interest rates. Making excuses and accommodating heavy debtors by keeping rates artificially low is one of the most damaging things you can do.

I really don't know if this is correct or not, but one thing I've heard is that low rates disincentivize lending by banks because loans are less profitable. Higher rates will actually encourage lending. Much of the money in circulation comes from the banks because of fractional lending and not from the fed's printing presses. I'm curious if anyone has a take on that.

Also, I think rates need to be looked at in comparison to GDP growth. High rates are fine when GDP growth is greater. If rates shoot higher because the fed is trying to stop runaway supply-side driven inflation while GDP growth is low it could easily kick off a depression.

Higher rates increase willingness to lend. Lower rates increase willingness to borrow. You need both a willing lender and a willing borrower for lending to happen.

Spreads compress when rates are low, so yes, loans are less profitable per dollar when rates are low. But many more people and companies want to borrow so banks make out fine. And there are plenty of other financing sources available for companies, including issuing equity, VCs, junk bonds, which grow in popularity when investors need to chase yields.

Even worse than rising interest rates is a society addicted to the fentanyl of zero interest rates.

There is a reason major religions regulated debt in general, because that is how societal slavery develops. Of course we, the modern people of technology, 'know better' than our primitive ancient ancestors.

I don't get it. Most religions were against usury and they insisted on debt forgiveness if the debtor can't pay.

Charging 0% interest is absolutely fantastic. The only problem is that we don't do the debt forgiveness. We bail out banks and then expect tax payers to shoulder some or all of the losses. It was especially bad with Germany vs Greece. German banks were bailed out and public healthcare was basically eliminated in Greece.

The only reason why anyone would be against low interest rates is that they noticed that those interest rates eat into economic rents and therefore the owner of money benefited from the economic rents rather than the owner of the monopoly.

In that sense, the only difference is that the money goes to the land owner instead of going to the bank. People don't realize that if they buy a $600k house with 0% interest that they would still have to pay $600k at 5% interest except most of the money goes to the bank instead of the seller who only gets $250k (made up number).

I think people forget just how bad the early 80s recession was, possibly because most of the people affected then are dead or senior citizens now. Nationwide was 10% (on par with the 2009 recession), and in some cities it went up to 25%. Farmers drove their tractors into Washington DC and blockaded the Eccles building. Car dealers sent coffins containing the keys of unsold vehicles. Construction workers sent 2x4s to Volcker because nobody needed them for home construction. The Treasury Secretary publicly undermined him, and the House Majority Leader called for his resignation.

Sure, but the mortgage rate was around half that in the year before and just as high in 1974. Though compared to today, 13% is high but not ridiculous. 13% today would be ridiculous.

Canada already did #2. Average home prices in almost all metro areas are around 10x yearly income. There is no blood on the streets and it is still considered a destination country.

it's human nature and backed by human history. blood on the streets will come, maybe tomorrow, 10 years from now or 50 years from now. in the face of inequality, it's either war or fascism. no two ways about it.

My Canadian friend mentioned this but then followed it up by saying no one in Canada cares what the Bank of Canada does and all eyes are on the US. Could that be one reason there wasn't a significant effect?

Also, there's quite a bit of cash in savings accounts now, and rates are still low by historical standards. We'll see what happens when mortgages are above 5% again.

10x isn't terrible, though, is it? Assuming 20% down on a mortgage, if you're frugal, you can save for a down payment in 4 or 5 years or so. Not ideal, of course, but not impossible. In some places in the US folks could save for a decade or more and still not be able to afford a down payment.

3x is based on early-80s interest rates (12%). I did out the math [1] for someone on Reddit and it turns out that if you buy 3x your income @ 3% interest, you'll only be spending about 12% of your income on housing. To get to 30% of gross on housing (the other common rule of thumb), house prices need to be about 7x income.

3x is not based on 80s interest rates. And the mortgage is only part of your expenses, you need to budget for home repair, taxes, and insurance. Plus any other savings that are needed, like putting yoyr kids through college or retirement.

I did out the math in the Reddit comment, and you can run the numbers by Googling [mortgage calculator] and plugging them in. 12% is the equilibrium interest rate where the "home price = 3x income" and "housing expenses should be no more than 30% of gross" rules of thumb are both true. At 3% interest rates, a 3x home will cost you about 12% of monthly gross, and 30% of gross will get you 7.5x income. Those two rules of thumb cannot both be true at 3% interest rates.

With taxes and insurance, those numbers change to 3x = 17% of gross and 30% of gross = 5.4x, assuming California tax rates. Things like emergency funds, retirement savings, etc. are included in the "housing should cost no more than 30% of gross" rule of thumb.

Housing expenses should be no more than 30% gross isn't a rule of thumb, it's a maximum amount lenders will traditionally lend you. It's called the front end ratio.

Quoting investopedia "Lenders prefer the front-end ratio to be no more than 28% for most loans and no more than 31% for FHA loans."

Lenders don't care if you can retire or if your kids can go to college, they care if you are likely to default on your loan. So I wouldn't take the front end ratio as personal finance advice.

The 3x income housing advise in not related to the front end ratio. 3x income is the max you should borrow (according to the advise givers, you are of course free to disagree), the front end ratio is what you can borrow.

There literally doesn't exist a 3x property where I'm from in Europe. I make almost triple what the average salary is, and shitty old properties start at 5-6x.

What? Save 2x (20% of 10x) your annual income in 5 years? What planet are you on where you think people can save 40% of their net income, let alone gross

And even if by some miracle you save 2x for a 20% deposit, what bank will lend you 8x income for the rest ?

There seems to be a possible, overlooked cause & effect in the current landscape:

If FIRE followers scale the strategy of investing and renting multiple homes, are they not limiting housing supply for other potential homeowners or exacerbating homelessness?

It is not just that houses are not being built, but that a shortage of supply is caused by the FIRE generation: buying houses as investments rather places to live, with the goal of living off on other people's rents or Airbnb, not paying taxes and leeching on society for the rest of their lives.

Would these houses even be built if someone is not paying for them. They are not leeching but investing. May be we could call it leeching when they form a cartel and start raising rent prices in unison (which only biggies like black rock can do).

They invest in housing specifically because there's a bunch of tax avoidance loopholes for small-time landlords. There's nothing wrong with honest investing, but tax breaks are for leeches.

If tax breaks are there to be availed, why wouldn't anyone avail them. Does anyone pay more tax than they are legally obligated to ? It doesn't make much sense because the house prices already account for tax breaks, low interest rates and high rents. If one is to voluntarily to reduce rent or pay more tax or take higher interest loans, they would just be making losses and won't be in business for long. Many of these are not individual choices. They are choices of the market as a whole. Of course you can certainly get lawmakers to remove these tax breaks but till then no sane person would pay more tax even if they are progressive leaning in beliefs (not to mention most tax money goes to military spending so its not like paying taxes is even good by default).

The tax breaks are popular because they're advertised as making it easier for people to buy homes; in fact as you say they get priced in and so end up pushing up prices and making it harder for people to buy homes.

"No sane person would voluntarily refrain from exploiting tax loopholes" is the same kind of argument as "no sane person would voluntarily spend money to avoid damaging the environment". In fact there are plenty of people with a decent moral compass who do exactly that.

Tax breaks are written for two major purposes: giveaways to influential donors and incentives to take certain actions.

Rarely are they exclusively the second, but landlords get to deduct the economic costs of doing business. Loan interest and property taxes cost money, buildings and fixtures wear out (but the land does not). Maintenance costs money. Landlords have the ability to deduct these costs of doing business against rental income just like every other profit-seeking business does.

Can you name a tax loophole for small-time landlords that you think is improper in the context of a tax system which taxes profits?

You're begging the question; the fact that regular people are taxed on their gross income while the rich get to be taxed only on their profits is a big injustice in the first place. But on top of that: that rental properties are usually an investment that grows in value, so that's where a lot of the expenses you mentioned actually go, but they're deductible as business expenses; unrealistically high depreciation is also often deductible.

> the fact that regular people are taxed on their gross income while the rich get to be taxed only on their profits is a big injustice in the first place.

In many countries (including the two I've lived in as an adult) regular people get to make deductions for stuff like the cost of commuting to work, work clothes or equipment (to the extent that's not supplied by their employer), etc. By "deductions" here I mean, subtracting this money[1] from their pre-tax income and have their income tax calculated on what's left. In effect, getting taxed only on "the profits from work".

Surely even the USA must have some similar thing?

___

[1]: Often implemented as a default deduction anyone can make without proof; if your outlies are larger, save the receipts and deduct the actual amount. This general-deduction-amount at least used to be high enough that most people benefited from just checking the box to use it.

You can deduct costs that are narrowly specific to your job. But for most regular people the biggest costs of working are the rent/mortgage cost of having to live near a centre of employment, and perhaps the cost of a vehicle which they use for commuting, and neither of those is deductible.

Assuming this is not sarcasm, why not make that extra buck and donate whatever savings you make to what ever cause you see fit. It's odd to trust the government to use your money more prudently than yourself.

The rise of passive investing and FIRE is just a natural consequence of the "infinite" bull market and resulting widening equality gap.

Whether it goes down in a gradient to common people like FIRE folks, or is strictly restricted to the higher classes, someone will position themselves to profit from the Fed policies. I don't see how they can be blamed. Blame the people that create these economic conditions, because they and their friends certainly aren't benevolently leaving profits on the table, they're grabbing everything they can.

Isn't it likely that this is happening at a larger scale by private equity firms, REITs, and other commercial organizations? I don't see how FIRE is anything more than a drop in the bucket.

People buying houses and renting them to others to live changes ownership stats but does not increase homelessness, at least not in an obvious way. If a housing unit is occupied by N people, that’s N people who aren’t homeless because of that unit.

Buying additional houses and then not renting them out would contribute to homelessness as that unit would be housing 0 people.

He might be referring to the problem that the landlord has a subsidized mortgage whereas the renter is paying by earning money from the circulating economy.

> The Fed at this point controls the whole economy

No, it doesn't. Congress has a lot more control than the Fed (in fact, a strict superset of the Fed’s powers), and definitely much finer, more targetable control, but they have a little more problems coordinating on action.

> and they have two options

They have a near infinite spectrum of options between two poles.

> Raise interest rates and stop printing

Well, the first. “Printing” is just metaphor.

> Crazy inflation stops, but asset prices crash and we enter a major recession or depression.

There is no real reason (though its a popular unsupported idea from some quarters) to believe that there is no distance between the tight monetary policy sufficient to acheive the first effect and that which will cause the second effect.

> Do nothing, keep printing. Inflation picks up massively. The economy keeps humming along but young people, including myself, are permanently priced out of home ownership and many other things

Again, very little reason to thibk the last thing is at all true. We had high inflation with a weak economy with stagflation in the 70s, and young people then weren't permanently priced out of hone ownership. More normal, strong-economy inflation isn't going to do that.

> It seems like they are going with option 2.

Tapering QE is not “doing nothing”, its taking the foot off the accelerator.

The OP's #2 is actually an exponential growth in money printing.

If the growth stops being exponential, it moves away from the target in an exponential way. If the growth just becomes an exponential with a smaller exponent, it moves away from the target in an exponential way.

In theory you could have an exponential that grows in a very slow, controlled way. On practice, it will get out of control, because nobody has any idea what the target actually is, so you either always correct towards it, or deviate.

The big risk now is that the fed waited too long. They could have already raised rates when the economy started doing better before delta hit. They would have had more ammo this time around, and the supply side driven inflation we're seeing might have been tamer.

If the permabubble option is so predictable, though, it should be easy to account for. Just empty your bank account and send all your funds to a stock brokerage and go all in on TQQQ (triple-leverage NASDAQ-100 ETF). Your gains should predictably outpace inflation and even real-estate appreciation so long as the Fed doesn’t prick the bubble by hiking interest rates like they did with the dot-com bubble.

This is why I think inflation is not as big a deal as it historically once was. It’s never been easier to convert cash to inflation-sensitive assets and back again. We could very well transition to a world where cash simply becomes a short-term medium of exchange and loses all purpose as a store of value. All your wealth could kept in hard assets until the very moment you need to spend it.

Note that this is exactly how countries undergoing hyperinflation operate. Nobody keeps savings in the national currency, and if they do, they don't have savings for long. They keep their wealth in stocks, gold, foreign currency, bottles of alcohol, bullets, or any other durable liquid asset.

I don't quite understand the obsession with homeownership.

If a large enough percentage of people rented from property management companies, there would be more impetus to have strong tenant's rights laws to protect residents, and people would have more flexibility to move around. Moreover everyone would have an interest in increasing supply to keep their own rent down, pushing prices down toward cost-of-materials and upkeep.

As it is people willingly submit to homeowners associations that are in many ways worse than the laziest landlord. I don't see what gets worse by just becoming a nation of renters.

It seems pretty simple, I can spend money to rent a place, and after 30 years (rent), have nothing to show for the money I put in, or I can buy a house (mortgage), spend money for 30 years, and then have an asset I own.

Not to mention the freedom to do whatever you want to your home / house without having to ask for permission, or being in a position of putting money into an asset that you don't own.

It's not that simple. Right now the interest portion of my mortgage, plus my property taxes, plus my HOA dues, not to mention maintenance and upkeep, is more than what I was paying in rent right before I bought my house. That money is "thrown away" in the same sense as rent is; only money going toward mortgage principal gives me something to show for it. It absolutely would have been more economical to rent than buy. But I wanted to buy (see: your totally valid argument about having the freedom to do whatever I want to my home), and was lucky enough to be able to afford it, so I did it.

Sure, you can make the argument that I can hopefully expect some capital gains down the road if/when I sell the place. But that's not guaranteed (consider all the people underwater on their mortgages, for example, after the 2008 financial crisis; I wouldn't be at all surprised if something like that happens again during my lifetime), and it may well be that putting that money in the stock market would net me better returns over time.

But it really just depends on your local housing market. In some places it makes more financial sense to rent (rent < interest+taxes+upkeep), and in some places to buy (rent > interest+taxes+upkeep). And sometimes the financials aren't the #1 driver of the decision, anyway.