This isn't discussed much, but I think homes would become noticeably more affordable for families just by having the government stop subsidizing the mortgages of investment properties (e.g. only one mortgage subsidy is available for each family). This isn't even getting into tax write offs which are too complicated for me to understand the consequences of changing.

As it stands, mortgage rates being below the rate of inflation make housing a very attractive investment.

The sources of mortgage subsidy that I am aware of are secondary market purchases:

* Federal reserve mortgage purchases

* Fannie Mae/Freddie Mac mortgage purchases

A big portion of quantitative easing by the Federal Reserve is buying billions of mortgages every month. The Fed is trying to start unwinding this now, but they have had trillions of mortgages on their books since the GFC.

The subsidies aren't the root of the problem. It's municipal zoning laws. Just look at Japan. Went from having the worst housing bubble in world history to affordability in 20 years thanks to sweeping zoning reform.

Your point should be a pretty easy hypothesis to test, you may not know this unless you are from Texas but Houston effectively doesn't have zoning laws.

Cost of living calculation between Dallas and Houston says costs are roughly 15% different (as apples to apples a city I can identify to isolate zoning effects). So definitely some effect and a good lever to pull (in addition to others I am sure.)

I agree that zoning reform is part of the issue, I think zoning reform combined with other tweaks would go a long way.

I think that multiple issues cause these problem, we have runaway negative feedback loops in multiple areas, the problems has evolved organically over time so I doubt any one factor is enough to resolve the issue (as nice as that would be.)

I'm not making the assertion that zoning is the sole issue so I don't need to defend it but I figured I could take a quick look and bring some numbers into the mix so we have some numerical grounding for conversation and exploring the problem.

I lived in the Museum District/Third Ward in Houston for almost 2 decades now. Houston definitely has zoning. We just don't call it zoning. In fact, in addition to stealth zoning, we have neighborhood based facility also where even people in a neighborhood can tell you to piss off.

I'm not familiar with the ordinances in Dallas, but I think this may not be as much of an apples to apples comparison as you imagine if the thesis of that comparison is that "Houston has no zoning".

You have to find an actual free city to do the comparison.

So, I've lived in both Dallas and Houston (and Austin). Zoning has nothing to do with the price delta. It has more to do with employment, jobs, income, etc. The market will charge what the customer can afford kind of thing. Same reason RE in Austin is much higher than Houston or Dallas. It's all about tech money and influx of wealth from coastal cities. This is not COVID, it's just Texas - although, the supply shock really threw things out of whack. Years prior, we always did good enough to keep supply coming online at a reasonable price. Shutdown, commodity prices, supply chain, etc destroyed that and prices.

Anecdotal, but Greater Houston differs from DFW as it's more blue collar and DFW tends to be fairly white collar/corp focused. Ironically, Houston also has much more wealth. So what this means is DFW feels like it IS middle class with some lower, some upper, and a few Mark Cuban's. Houston has a whole neighborhood of Mark Cuban's, you see lower income everywhere, and it's kind of unclear where the middle is. In the exurbs? Is exurb A a middle, upper middle, etc. it's not clear where those lines get drawn. Dallas in particular is more segregated on income (which is correlated with.. you know) with the southern part of town being almost exclusively lower income. Houston is more integrated in this regard, there are pockets of wealthy areas surrounded by lower income areas and the folks interact with each other.

I actually don't hear a ton about the big money buying here in Dallas (Zillow, etc). It's just people that sold their west coast house for $2M+ and move here cash rich. I see a lot of mid-lifers so school district & distance to office is the biggest draw for which areas are seeing the largest price gains.

Not only this, but clearly whatever zoning laws are in place are not hindering new home construction in and around Dallas. Uptown, Deep Ellum, Design District have all had enormous booms in the last few years near downtown, and Cedars is currently having a new home construction booms. That's effectively every neighborhood anywhere near the city center. So it's not like you can't build new housing inside the city limits. The biggest factor delaying the projects right now is it's too easy to become a homebuilder, so many of the people don't know what they're doing and are way behind schedule. There also seems to be a shortage of licensed tradespeople. But it isn't hard to get approval to build.

Agree, zoning laws here are not meant to hinder new construction just control it's use. However, permitting went from ~30 days to about 6-12 months in Dallas. Supply is still causing a shock and construction just takes longer now as materials get delayed, etc. and it messes everything up. The trades are less capacity. They stayed busy though lockdown, or moved back to their native country to ride it out. I know several that just never came back. There are a lot of contractors turning builders, some delay due to their inexperience, but I don't see that as a widespread issue. But all in all, you see a lot of construction around but it's actually probably less finished goods than what was occurring in 2019. The lack of property and prices means people are building on any dirt they can find. I've seen some insanely horrible tracts of land get developed because all of a sudden, prices being what they are, it now finally makes sense to invest $250K in dirt work. I've seen land that has been for sale for 10+ years due to nobody wanting a 100% flood zone get developed in the last year; again because there's nothing better available and people have the $ to fix invest in drainage.

Dallas itself is competing with it's suburbs, Plano/Frisco etc. The development you see was planned 2+ decades ago and really only a surprise to folks that don't keep up (most people, I know, but I tend to keep up with this stuff and like to buy and hold land ahead of development). Bishop Arts for example has been a 3 decade overnight success, similar story with other areas you mentioned. Many of those areas I felt like they took way longer than they should have to get developed, and it's because all money goes north to the burbs. Uptown is about as far south as most money is willing to go. Design District, Deep Ellum, Cedars are proximity plays after Uptown got kind of expensive.

I don't really do much nightlife stuff. But about 10-15 years ago, Uptown was like the young professional/college kid place to be. Many of those folks moved to the burbs after a certain age. But many stayed. Now the prices are high, it seems like it's more full of those same folks that never married, never had kids, etc and just happen to be 10-15 years older. I think it still has the reputation but realistically, younger crowds (<30 or so) don't seem to spend much time there anymore in favor of Deep Ellum, etc.

My understanding is that japan does have historically protected districts, they call them preservation districts. I think it would be really helpful to have someone actually dive on the details.

Houston does rely on a lot on developers being able to put "deed restrictions" in place, which seems like their free-market/libertarian/state enforced private contracts solution.

I'm not familiar with Japan but their property laws are not unregulated so I think it's worth sussing that out so people can properly back their assertions with arguments and maybe we can derive a defendable % cost impact from zoning laws.

Japan has serious zoning law, but the issue is that it's reasonably scoped zoning that doesn't do things like "only single family homes here, no commercial properties including ban on corner shops" - they define what could be termed maximum allowed nuisance level, and the defined categories create a spectrum with overlap at both ends of each category. Even category 1, low rise residential, permits low-rise multiple units, small offices and shops etc. as well as certain public utility buildings (schools and the like). Compare it with zoning (or zoning hidden under other bylaws) in USA where you can end with a big area that permits only single family houses - no shops, not even a small grocery store, etc.

Do you have any examples of buildings like this, I've looked but can't find examples online? It seems zoning has a 15% overhead (all things being equal and as best as I could argue with the data I've found so far), maybe it's higher but I haven't found articulable/shareable evidence of that yet. IANAL, so hopefully an expert on HN can help chime in.

I've looked (links below) and have done more querying than a comment thread like this probably warrants but wasn't able to find your assertion articulated anywhere.

Neither Japan or Houston are unconstrained free-markets without land use control so I'm doing my best to roughly/quickly tease out zonings isolated impact on affordability. Neither locations have 0 laws so they are close to apples to apples and since we're just doing relative comparison I'd rather keep things data driven. Houston has deed restriction but that is a simple free-market/libertarian private contract solution. Does Japan ban deed restrictions? Both japan and houston have historical zones

I've linked these two jstore articles as well as a more digestible video.

If there's enough bylaws that the only building you're allowed to build is in the shape of a SFH with a driveway, that's the only thing that will get built

Houston has a lot of other land use restrictions. I should have been more specific. Even without zoning, you have rules like floor-area-ratio, parking minimums, setback requirements, etc.

Tokyo actually isn’t growing that fast in population. They just construct a lot of homes there because the Japanese don’t like to buy second hand ones (so tear down the 30-40 year old house and build a new one).

40% of homes in my city were bought by institutional investors with basically cash offers that no one can compete with. They openly state the point is to corner the market on a scarce resource and drive up rents which are also up 30+%. This is clearly a problem zoning or not.

The zoning laws didn’t change in between. Japan got burned on property speculation, and no one no longer sees residential real estate as much of an investment. Also, no one wants to buy second hand structures, so your appreciation is limited to land and the existing housing on that land is a liability (buyers have to tear it down before building a new house on the land). Japan has a large amount of housing starts because they have a large amount of demolitions. Liberal zoning allows for this, for sure, but I’m not sure many Americans would be willing to go that route.

2) Unfuck building codes. Person signs their own death warrant? Let them live in a yurt or a the kind of shack people keep their garden tools in. There's a county east of Tucson like this, guess what, people no ded.

3) End all subsidies and government involvement in mortgages. Best way for skyrocketing price is for government to guarantee loans in a way a relatively free market would not.

4) Permit fees dropped for building housing. Cost of evaluating permits should drop without zoning or building codes. Only examine development to make sure it doesn't cause imminent harm to those outside the property line.

Zoning fixes are absolutely required, but Texas (particularly Huston) is not a good model. While many places in Texas don't have so-called 'zoning' they manage to implement pretty much all the restrictions zoning reform advocates want fixed through things like land use restrictions on deeds (which are even tougher to reform than zoning)

Japan is the model I'd like to see: inclusionary zoning. A small number of zones that allow for maximum use.

This might have the opposite effect. Permits and building codes are there for the lender. They want assurances that the property is going to last for at least the duration of their loan. If lenders decide these deathtraps aren't worth the risk, and they have no way of offloading that risk to someone like the government, they aren't going to bite.

The entire housing industry is designed around lending. If policies are make that screw with the status quo, the industry is going to collapse then reform around the new one, and that could take decades.

We have regulations for a reason. When you blindly get rid of all of them, history repeats itself. We find ourselves looking to solve the same problems. It wasn't that long ago in the USA when entire cities would burn to the ground because a cow kicked over a lantern because lack of building codes meant buildings weren't built with safety in mind.

> Permits and building codes are there for the lender.

Aight, so if I'm the lender for myself let me nix them. If they're for some third party lender, let the lender and lendee solve that through private market rather than government. Surely someone can be trained to inspect a house.

> [ mention of Great Chicago Fire ]

The classic "make hundreds millions of people work for decades to afford a house, costing tens of millions of lifespans of work so we can save 300 people once a century from the great Chicago Fire". The calculus there is way way way off.

I'll take my chances.

>It wasn't that long ago

It wasn't that long ago housing was far more affordable.

> because a cow kicked over a lantern because lack of building codes

You've fallen victim to a big tale, like santa clause. No one knows the cause of that fire. We do know that many of the conditions were completely unsubject government, such as a windy dry spell.

>We have regulations for a reason

They're there for good reasons, unfortunately the worst tyrannies and misdeeds happen at the gunpoint of those who purport to be acting for the common good. Building codes in practice are as much about taking your life away as they are as preserving it.

Building codes aren't nearly so bad as zoning and the NIMBYism that is strangling the country. There's certainly room to liberalize building codes, but I don't think the impact would be as large as one might hope. Liberalize land use please.

Everything you just wrote sounds like a good thing to me. The fact that housing is structured around lending in the US is part of the problem. It should not require a loan to get a roof over your head, and combined with zoning making basic housing illegal, there's a lot of perfectly sound shelter that cannot be legally constructed in the US.

I believe that one of the things that make Texas more affordable is high property taxes. It keeps people from borrowing more money and competing as aggressively on price. So they pay in Taxes what they would be paying in interest. Taxes at least are spent in the community. Schools, roads, parks, etc.

Housing prices have little to do with property taxes, just in how the amount levied is paid by homeowners, not in the amount levied. The reason property taxes are high in Texas is for the same reason they are high in Washington state: no state income tax. That doesn’t really keep our housing prices low, however.

Texas sucks just like almost everywhere else. Oregon's reforms we're pretty aggressive though. The entire Portland metro area is zoned to at least quadplexes in residential areas, and duplexes statewide. No SFH zoning allowed. California I think only made the minimum two units.

I think it could be greatly simplified by holding the building owner/manager criminally liable for defects that lead to major injury or death, and civilly liable for smaller defects.

There's no reason for the government to have an opinion about what type of concrete you're using or how many feet of wire you're using. They should be policing outcomes, not hiring and sending inspectors all over. If a building collapses, the people who own it and the people who built it should go to jail.

And insurance companies can come after the owners for the smaller problems.

How is "let the building collapse then send the owner to jail" an improvement over "don't let the building collapse"?

Why would we get rid of building codes, but then still jail people who don't follow the old building codes that we just got rid of. All this would accomplish is sending well-meaning people to jail, just because they didn't know their house had a serious problem, because we got rid of the building codes.

The argument is probably something along the lines of "most building codes are costly but not necessary for safety" aka "it can be somehow done significantly cheaper but just as safely, a way that doesn't follow the building codes".

I guess it comes down to comparing the risk of poor quality housing vs the risks of homelessness. Kind of like that saying "the real minimum wage is zero"

For many of those people, it's not a risk of homelessness but rather that they would have to rent someplace outside the favela at a much higher price, one they may be able to barely afford. Sort of like in the US, where zoning/building don't generally make people homeless but instead put a person into the situation of the favela dweller who has the option to rent while paying a large portion of their income, except without the option to build their own sub-code housing.

No one wants liability. Builders wants to build and be gone ASAP. They'll build a $350k home using the cheapest parts and labor they can find and do their best to run away with the profit. 5 years time, after any sort of warranty, their workmanship (or rather, their lack of it) starts showing.

I think your idea would be great, but there would be turmoil while the liability hot potato is thrown around until the industry figures out where that lands (probably some form of "malpractice insurance" on builders would become a thing, with higher premiums on those who suck more, eventually forcing them to be better or quit entirely).

I’ve developed a heuristic where anytime I hear phrases like “affordable housing”, “make college affordable”, “affordable healthcare” I simply translate it to “unaffordable”.

Inevitably when these become government programs, they simply throw money at the problem without addressing fundamental supply and demand issues and accomplish very little except drive up prices. Then, when investors see prices going up and to the left, they rationally throw money at it in a way to make even more money, which drives up prices even more.

There’s a really good book I recommend called “Systems Bible” [https://www.amazon.com/Systems-Bible-Beginners-Guide-Large/d...] that beautifully articulates this phenomenon in a way that applies to government policy, software systems, management, org structures, or any complex system of people or machines.

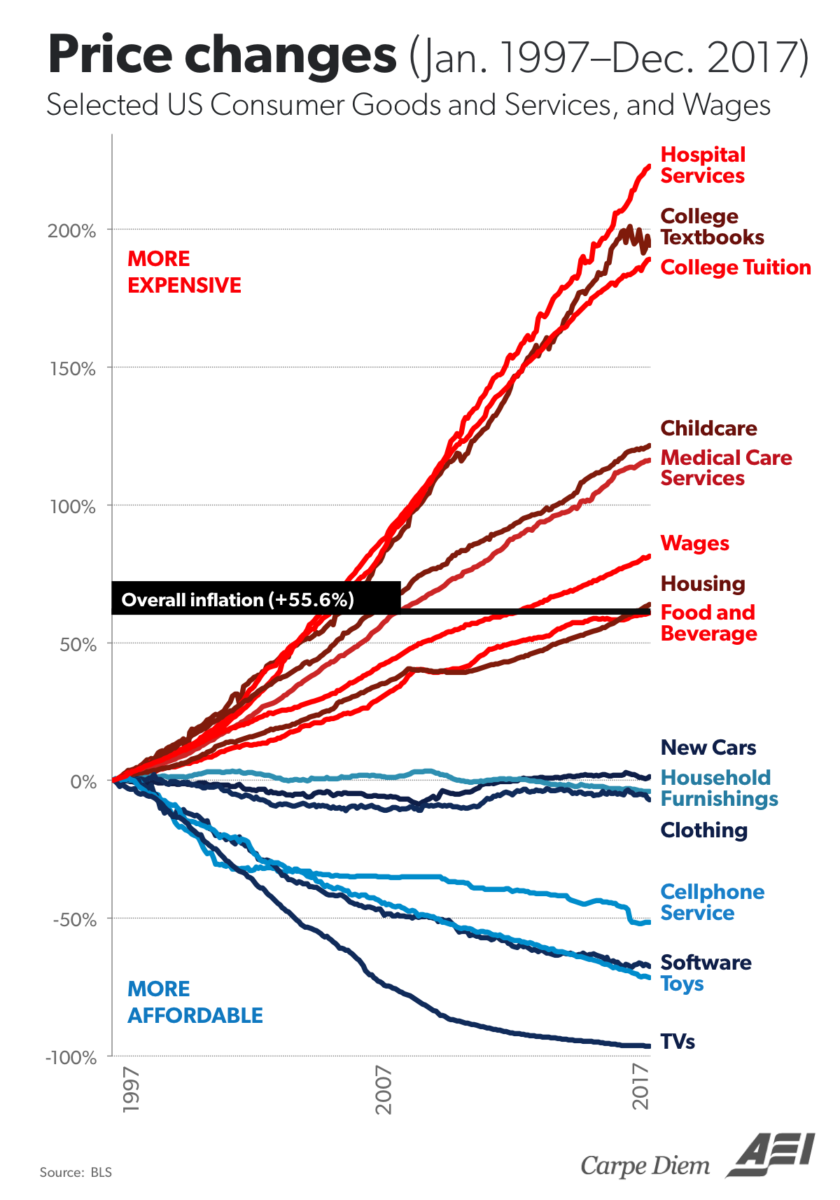

It's insane how these once affordable services like healthcare or university, that you could pay with a summer job, now take years off your life.

You may enjoy this article [0]. To quote from it:

> In the past fifty years, education costs have doubled, college costs have dectupled, health insurance costs have dectupled, subway costs have at least dectupled, and housing costs have increased by about fifty percent. US health care costs about four times as much as equivalent health care in other First World countries; US subways cost about eight times as much as equivalent subways in other First World countries.

That would require a much larger change to the tax code as currently interest on business loans are tax deductible. I suspect changing this would be a good idea, but it’s a huge change.

The obvious fix is a nationwide property tax that doesn’t apply to primary residences, but again it’s hard to say what that would do.

Somehow there need to be less incentives for investors/hedgefunds to buy up homes and more help for people who need housing and are increasingly priced out of the market. Housing affordability is a serious crisis right now and neither political party seems to be recognizing it. The party that makes this a priority and actually addresses the underlying problems could do well, but neither of them are taking it as seriously as it needs to be taken.

> Housing affordability is a serious crisis right now and neither political party seems to be recognizing it.

Why do you say this?

There have been numerous bills introduced at the local, state, and federal levels which specifically aim to address housing affordability. Seriously, just type in "affordable housing bill" into your favorite search engine and look at all the articles coming up from the past six months.

My local city council has affordable housing on the agenda for several of the committee meetings.

None of the local "affordable housing" actions I'm seeing seem like they actually address the problem at the level it needs to be addressed. They give incentives to developers to build a certain number of "affordable" units which must stay "affordable" for X number of years for them to get their tax breaks. In the meantime they build a lot more high-end units and very few mid-level units. Mostly this seems like a gift to the developers. Do we get some more affordable units? Yeah, but it's a drop in the bucket and after some number of years they can go back to market rate. People are on waiting lists for these "affordable" units for years. These units are reserved for people making some percentage of the poverty level income. People in the middle get nothing.

In my area/state they've dropped most of the zoning restrictions for locating apartments and ADUs. So you can add an ADU (a small dwelling that can be rented out), but that takes capital that most residential homeowners don't have. Add to this the fear that by building an ADU your property tax will likely go up very substantially and there aren't a lot of takers.

tl;dr Most affordable housing efforts are currently aimed at people who make poverty level incomes (and that's great). I don't see much locally aimed at providing housing that's affordable to folks in the middle. And as rents rise, more and more folks in the middle are not able to afford housing.

That indicates a lack of understanding of how to solve the problem (or, at the very least, a disagreement with you about how to solve it), not a lack of recognition that there is a problem.

You get affordable housing by building more housing not simply designating a percentage of housing to be affordable.

If anything current affordable housing initiatives just make things worse by discouraging new development. Building 10,000 new apartments is strictly better than building 5,000 apartments even if you designate 30% of them to be affordable. The ideal solution is to designate minimum density, so for every acre of land you must have at least X homes.

Wouldn't the obvious fix be elimination of 1031b exchange, capital gains on all house appreciation, and only allowing 1 active federally backed mortgage at a time (with some consideration for allowing a purchase of a new place & selling the old place).

The land appreciates without development on it. If anything, we want only appreciation from developing. If you don't do something to the property, you shouldn't get a profit from it

I think that’s what they where suggesting, however that’s really expensive and hard to implement. If you simply calculate based on the value of the land then a 200 year old house counts as “new” development etc.

Worse it doesn’t actually help. The incentives are there to develop land it’s only local zoning that prevents it.

They've eliminated this deduction in both the UK and NZ in the past couple years, at least for individual landlords. NZ does allow it for new builds to incentivise construction of new housing.

Big landlords already incorporated in the UK. Small landlords (the majority), who haven't yet, just move in that direction and get screwed with legal and accounting costs, but otherwise nothing changes.

Most limited company buy to let mortgages in the UK are underwritten by a directors personal guarantee. It's just a technicality compared to a personal mortgage and so only shakes out the laziest of landlords

It’s a lot more complicated than that with a mix of short and long term effects. It should make home ownership more desirable, but taxes don’t destroy wealth so lowering income taxes for example could largely offset any increases in rent.

Further the value of property would decrease, but the cost of empty properties would increase. That would put downward pressure on rental costs.

> having the government stop subsidizing the mortgages of investment properties (e.g. only one mortgage subsidy is available for each family).

I think you are confusing home loans (which are subsidized) and business loans which are not subsidized).

Fannie Mae/Freddie Mac loans are only on 1 primary home and 1 secondary home for individuals. These loans are limited and really don't work in high property value states. You should google the difference between "conforming" and "non conforming" loans.

You might be thinking of the mortgage deduction on the income tax. Trump already did this. This only hurt young people in high property value states.

Business real estate loans are more expensive because they are not subsidized. However, businesses do pay taxes only on earnings (income-expenses). Loan payments are expenses that reduce the earnings. Good luck on getting rid of business expenses. Yang proposed changing the tax law because of this.

All this means your proposal would have a very limited impact. It would only hurt individuals who live in an expensive property where the homeowner has mostly paid off their mortgage (old people) and used the principal to buy a rental (up to 750k).

For Freddie/Fannie: some sources say that they support investment properties for conforming loans [1]. They have information about loans for investment properties that I am still trying to make sense of [2]. I have seen other sources say they support loans for 10 properties.

Even if the support were only for 1 secondary home, why should the government be subsidizing this?

I understand these policies work differently in expensive markets. But as per this article, investors are targeting rentals in less expensive markets.

Idk how this translates into policy if it's even possible, but people just shouldn't be so attached to home ownership. It's a not a great way to invest your money and it doesn't make any sense at all to tie your personal net worth to a piece of real estate you rely on to live. In high cost areas especially, renting is usually more fiscally sensible.

On the smaller scale, and for certain kinds of multi family purchases, government-backed financing is available and it is usually cheaper than what one might find on the private market

Not for the mortgage itself, but real estate investors typically pay very little tax on their rental income. You can take depreciation, and deduct maintenance/repairs, property management fees, property taxes, insurance, etc. in addition to mortgage interest.

Are you suggesting a business should pay tax on the gross income, regardless of their costs? A store should pay income tax on the gross sales, without deducting the cost of purchasing the things they later sell?

So if they increase interest rates, buyers won't buy the homes that would liquidate their balance sheet and prices would drop as well, undercutting the value of their balance sheet.

So what is the Fed's motivation to raise interest rates to curb inflation in this case?

Housing will never be relatively cheap until it’s easier to build a house. It will never be easier to build a house until zoning is more lenient.

No state is incentivized to make zoning more lenient. Therefore it falls on the federal government, who lack the authority.

The only thing they can do is something similar to what they do with the highways and threaten to take away funds unless all plots of land can be zoned for up to 4-family houses (FHA limit).

Potentially quadrupling the amount of housing will do it.

Zoning is an issue but there's also the onerous costs to building something today even when you do have the zoning to add capacity to a given lot. For example, you might notice every apartment you see has a balcony. That's because code dictates balconies for every living unit, meaning the build just got that much more expensive per unit just because some people on city council 50 years ago thought apartments with balconies were more seemly or something. There's also long review periods. It's typical even in growing urban areas to see lots bought for development, raised, then seemingly left to sit vacant for years sometimes even with earth-moving equipment or cranes laying idle, biding time, while the permits cycle through the purgatory that is the building office in city hall.

This is all the result of corruption. City councilmembers in cities across this country found themselves in the position of kingmaker. Decades of entrenchment of the political class saw this role refined, distilled, and now it's practically impossible to remove the layers and layers of ossified process that has corrupted anything we do. This is why housing is not being built, why construction costs on projects are so high, why timetables of doing anything at all are decades out, and why the FBI indicts major local politicians for corruption every year. Decades and decades of systemic corruption that has not ever been rooted out has led us to this current broken state.

> Decades of entrenchment of the political class saw this role refined, distilled, and now it's practically impossible to remove the layers and layers of ossified process that has corrupted anything we do.

I would love to see a federal regulation stating that any housing construction permit that isn't reviewed within ten business days is automatically approved.

Not all states are that bad. In the midwest things tend to be approved much faster. Which is why our housing costs are not as bad as CA (still not great, but they much more reflect the cost of building)

That's because there isn't usually enough demand to really set up a good building office greasy palm operation, but corruption certainly happens there too (Cuyahoga county has seen issues over the years and Chicago alderman corruption is legendary). If you don't have demand, onerous building process will just turn developers away and they will opt to build somewhere with about the same demand and less process. Sometimes that's even used as a tool to quiet development on purpose. If you have a situation where there is a lot of demand, like in the bay area where they've added 7 jobs per unit of house constructed over the past decade generating huge latent housing demand, councilmembers know they can make the process as slow and unforgiving as they want and developers are still strongly financially incentivized to build to meet this huge demand, and not only will suffer through the process but will often actually pay the councilmember a bribe or echange favors in some way to speed up the wheels. The more obtuse and complex the process, the more levers a corrupted official can pull to speed things up or slow things down and keep it looking like routine process on the face and out of the press, until the FBI finally gets prosecutable evidence of quid pro quo and puts in the indictment.

Yes, I'm really disappointed to see so many other comments here that misidentify this fundamental problem. Investors are only interested in housing now because prices were already rising thanks to constraints on building due to zoning.

These investors aren't the ones making the prices higher (or they weren't initially, at least); they're responding to conditions that were already making prices higher, which makes their investment more attractive.

But you don't have to take my word for it; it's literally what they say in their prospectuses:

Everybody has their favorite group that's easy to hate in this space -- it's the vacant investment properties, or the foreign investors, or the REITs, or the rich people with vacation homes -- but those are tiny factors relative to the main driver of this, which is your typical one-house-occupying all-American homeowner who opposes any new housing in their neighborhood.

Exactly this. Investors aren’t buying up housing for fun, it’s because their investment thesis tells them they’ll make a lot of money.

As soon as the prospect of housing appreciation disappears so will the investors. But then we’ll have sad stories about people being underwater on their mortgages.

Massachusetts is trying to force Boston suburbs to lift single family restrictions. Great intention, though i have feeling each town is going to fight for years against it.

It's not compulsory and it's not lifting, only requiring multifamily zoning around transit catchment areas. Towns that refuse to implement it lose out on state funding meaning the wealthy towns are free to ignore it. Perversely, those towns will now cost even more to live in because they need to offset the lost state money.

> No state is incentivized to make zoning more lenient.

Zoning is largely a local issue. And zoning is talked about a lot at local council meetings. The problem is people have very strong opinions when it comes to how the place they live will change. It's trivial to get a sizable contingent of people to oppose zoning permits.

There's a huge argument going on a few towns down from me as to whether a 100yo, vacant building in disrepair should be torn down to make room for a community center. One would think this is something obvious that would go unchallenged by locals, but nope.

Making zoning a state issue would probably help a lot, but it would piss off home owners. Even early champions of the change are going to hate it when their neighbor's houses get torn down so that a casino or something can be built in their place.

>Making zoning a state issue would probably help a lot, but it would piss off home owners.

Given the current situation in many state governments, this would have huge ramifications. You might live in a mid-size city and have the wingnut state government refuse to let you build any more homo-muslim-crack housing anywhere in the city center. Or the rural/exurb dominated state house will only let you build a unit in downtown if it comes with 3 parking spots large enough for lifted Ford F350s.

Personally, I live in the South in a city where local politics are dominated by the suburbs and it's bad enough already. "Not enough parking downtown" because you might have to walk 3 blocks to the nearest street parking lot, so of course more lots must be subsidized. Huge portions of downtown taken up by 6-lane corridors impossible for pedestrians to cross so that suburbanites can zoom through at 50 MPH. And that's set up by people who live and work 20 minutes away! Imagine the situation if zoning and city planning was primarily determined by car dealership scions who will never come here in their lives.

> Even early champions of the change are going to hate it when their neighbor's houses get torn down so that a casino or something can be built in their place.

Even the strongest critics of the status quo don't think we should eliminate all zoning, so that you'd be able to put a casino on a residential street. What we believe is that you should able to build more residences (and maybe a corner store) on residential streets.

From what I see from zoning reform advocates, many look at Japan as the solution, precisely because in most of japan, residential houses can go in most any zone. Meaning, an old warehouse could be torn down and replaced with SFH without any change in zoning, but theoretically, a gas station or strip mall can be built right next to those same houses.

You can replace an old warehouse in the USA with SFHs. The major difference is the area will have to be rezoned completely before construction starts and the public will get their chance to voice their opinions. This allows everyone to agree on what else may be built on this land before houses go up. Will it be mixed use? Residential only? Are multi-tenant buildings allowed?

Then there's the big issue of who controls zoning? Should it be at the state or local level? Both have their positives and negatives.

What about the new elementary school and sewer lines they are going to need to convert an industrial zone into residential property. It’s not like Japan where we feel comfortable sending our kindergarteners off to the train alone to go to a far off elementary school. Oh, ya, we don’t have a train anyways so it’s even more complicated.

I agree completely. While its fun to place the blame for high prices on the investors, in reality the high prices are for the same reason that we see high prices of everything else: there is a shortage.

Zoning reform is a solution to get out of this mess, but zoning is not the only cause of this problem. If you look at the last 10 years of housing construction in this country, and you compare it to the previous 50 years, you see that we have simply not been building enough housing:

If a nation spends 10 years not building enough housing, high prices are what happen. If you add low 2020 interest rates to the mix, the effect on housing prices are explosive in the short term.

>No state is incentivized to make zoning more lenient.

All states are actually incentivized to increase their supply of housing, because an increasing population allows them to eventually gain greater representation in Congress relative to states with less growth. States like California, New York, and Illinois are losing out to states like Texas, Florida, and North Carolina.

Zoning laws are determined at the municipal level. It's local government that is the problem. State governments have actually started pushing reforms thankfully.

Exactly, this is one of clearest examples I know of where small, local government backfires. For example, my small town recently passed a law allowing all homes to have an accessory dwelling unit. Come to find out the only reason it was passed was because the state required it by law. But within my towns borders there's an HOA that doesn't have to allow them, since of course HOA's are a loophole to the law. I imagine more HOA's are going to start appearing.

I don't think it would take quadrupling. It would take adding enough housing that housing quits being a good investment for investors, so they stop buying up houses and start selling the ones they have. I suspect we reach that point long before we quadruple the supply.

Why? Because investors would have more and more houses sitting empty. That would force a change fairly soon... wouldn't it?

The people electing the officials that make these policies are the ones that want to keep low-density housing. It's suicide for a politician to sponsor rezoing legislation.

We're in the housing hunt right now and we're losing to all-cash offers and ridiculous terms (like months of rent-free to the previous occupany: those sort of terms don't come from someone looking for a new place to live). We even lost on two offers where we were the high bid. We have pre-approval, solid financing and were willing to even waive the appraisal. It's not enough.

Also on the housing hunt and have had the same experience. It's really disheartening to tell someone I'm going to give you exactly what you are asking for and have that transaction, that seems so easy without any kind of counter-offer back and forth, fall apart... multiple times. An article like this definitely brings out a little anger.

You said it. One of the most galling things was sellers' agents that don't even let your agent know that you didn't get the bid (let alone ask for counteroffers). We only found out we lost out a couple times when it went pending on the MLS; we never heard a word. We're just interchangeable piggy banks to these people, apparently.

Been house hunting as well. You know what I've seen more than ever? Seller's agents behaving as jerks. Things we experienced going to open houses:

- Agent sizes us up (I dress down on purpose), says something to the effect of "You know this house will probably sell for even more than (already high) asking".

- Agent just sits around playing with her phone. No shits given.

- Agent sizes us up, realizes we're just window shopping/taking our time, "mansplains" to us "you know how this works, right? 24 hours from now there will be multiple offers and it will be gone"

The other unfortunate thing right now is that loan rates are (finally) spiking. Like > 4% for 30 year fixed. I wish we bought before the winter... And even worse if this keeps up the housing prices will crash just when we bought high. Oh well.

I hate to say it but when you are on the selling side and you are getting all sorts of offers, you just go for the most money and the easiest closing (in most cases). Then it's your turn to enjoy the buyers side of the sellers market... Unless you've decided to just rent for the foreseeable future with your newly attained cash horde.

Do you expect things to get better in the future? I'm not in the market to buy right now, but I'm trying to understand if the current situation is the new normal or still a reaction to covid upheavals. My gut tells me that in 2-3 years things will be much closer to normal as rates rise and people that fled to suburbs decide to move back to the city.

My theory is that places that are inherently more desirable, whether because of culture, geography, or employment opportunities, will remain high. This probably includes most coastal regions and trendy inland spots (Austin, Boulder, etc.).

I think a lot of 'secondary' markets could take a hit. These are places that the main appeal is their current relative affordability or proximity to a more-desirable area. I think buyers that are priced out of 'desirable' areas today are effectively settling for these secondary areas, which is raising those prices. I feel like those will be the first areas to take a hit. How big that hit will be, I certainly can't say. It could be as little as a reduced rate of property appreciation, or it could be as large as a 20% hit.

I'd expect a lot of this depends on where you are. Some places it won't matter a whole lot what happens with Covid/rates.

Friends in the DC region aren't worried as this has been an ongoing trend for quite a long time (they have enough equity that a dip won't matter much). Friends in Southern California would probably say the same thing. But in Phoenix, I already hear some questions as to whether this will come tumbling down in a year or two.

Myself, bought a place (not a city and not quite the 'burbs) last year and I'm still curious about my local market so I still constantly check the real estate sites/apps just to see how things are moving in my area. Would suspect I'm not alone in doing this.

My assumption is that a large percentage of the people who fled NYC/SF in March 2020 are either 1) going to miss the city once it fully reopens and they remember why they lived there in the first place; or 2) their "remote forever" job is actually going to become hybrid and they won't want the 2 hour commute.

Probably not. The majority of the tenants in my building are young professionals and empty nesters. Families with children come through but are gone after a year. Once you're on that track it's very hard to go back to city living. Space is at a premium and kids need space for 18 years. I assume the suburbs are made of people that love suburb living (so much space!) and people with children.

Outside of finance and government there isn't a large sector in most cities. Most businesses are in cheaper, suburban office parks. So beyond the social and cultural aspects there aren't that many advantages to city living, IMO.

I'm sure some people will return to cities, but I feel that many will remain in the suburbs. To me, one of the pieces of this surge in prices is due to millenials reaching prime homebuying age. But millenials are also at prime ages for starting and raising families, so I suspect many will prefer to keep the larger size of their suburban homes.

Sometimes (or often?) mortgages and financing can fall apart at the last minute, so sellers often prefer all-cash offers because they know there's virtually nothing that can make the deal fall through or drag on long. Pre-approval is usually done by different people than much stricter people who do the underwriting, so things can fall appart there, too.

When I bought my last house (newly built), on the DAY OF closing, 2 hours before the closing appointment, my mortgage officer calls me to tell me I'd need to bring another $5000-ish (due to a reason I've blocked from my mind). He told me my builder would bring a check for an equivalent amount made out to me, but to make the accounting/financial all legal, we couldn't just "zero each other out". The money had to clear from both accounts. (I wish I could remember exactly the circumstances). And, this money couldn't just be a check but had to be a cashier's check that was guaranteed. It couldn't be cash, either, because it had to be from an account that the underwriters had reviewed and done money laundering screening for.

Due to the logistics of that day, I had to go through herculean efforts to get that cashier's check made. I usually bank with online-only banks, and thank god that I had a local bank with just enough balance to make it all work... And that's for someone who is lucky enough to be able to bring that extra money and to be able to take the day off of work to make happen. I imagine many others wouldn't be as lucky.

That closing could've been easily pushed off a couple days had this surprise made us unable to close that day.

Sellers like not dealing with this, so they prefer cash offers.

It de-risks and accelerates the transaction. Most mortgage based purchasing requires the loan lender to approve the house for the value (even if you are 'pre-approved' for a loan of $X, if the bank doesn't think the house is worth $X it won't let you take the loan out for it). All cash offers don't have those approvals or risks, however slight, and also have no/less time delay - you can close in a week (just a title/deed history search, generally).

Because with cash you have the money to actually make the deal happen. With a mortgage you depend on a bank giving you the money.

A bank says they will lend 75% LTV, you are preapproved for a $2M house, so will bring $500K to the table and bank will provide $1.5M you think.

But wait, the appraisal comes back for $1.6M instead of the $2M you bid. Bank says no problem, we will lend 75% LTV or $1.2M. Now you have to find (within days) $300K. And you can't borrow it because that will mess up underwriting on your current loan.

Or you buy a car before closing. Whamo - your DTI is toast.

Or you have someone open a CC in your name. Whamo - no closing.

One reason I can think of is because the bank does an appraisal and may reject the loan if the appraised price is too low. They don't want to be stuck with a house worth less than the loan. I had this happen several years ago with a house I bid on (I was also pre approved and all that stuff).

Time to close a loan is couple of weeks at the very least (could be 4 or more). The cash offer closes in days. Sellers prefer the latter: bis dat, qui cito dat.

What kind of mortgage allows you to waive the appraisal? Seems a little negligent for the bank. How can they finance something if they don't know how much it is worth?

No, you waive the appraisal contingency; the bank still does their own appraisal. If the property appraises low, you pay the difference. In this market, we kept some reserve for that eventuality to make the application competitive. The sellers want a buying frenzy and that's what's happening, so many properties don't appraise since those values are usually calculated on historical sales.

The bank will only cover what it is appraised at. You have to split the difference with cash. Some banks might be willing to give you different terms (higher apr, more down) but that is generally how it works in my experience.

I'm in this boat too. It feels like a line was drawn sometime in 2020 or 2021: either you bought before then, and now you can enjoy your appreciation and relatively low mortgage, OR you're currently desperately trying to grab onto the last rung of the ladder as it gets lifted above you.

Regarding all cash offers, have you looked at all cash options that are available through lenders like accept, inc [0] or better.com [1]?

I’m in the market for a place now and recently lost to an all cash bidder. Turns out they were using [0]. I was already pre-approved through a conventional lender, but all-cash seems to be the new norm.

pre-approval doesn't amount to much. One thing you can do to compete with cash is to get a fully underwritten mortgage (you need to find a lender that does this). For a fully underwritten mortgage, the lender will give a $10,000 guarantee that the mortgage will close: this makes the offer more similar to a cash offer.

These still have lots of stars. They will close IF property appraises at value you bid. Heads up, in a multiple offer scenario it very likely WILL NOT.

I went though exactly that, and it's disheartening, indeed. I was fortunate enough to finally get my financed offer accepted, but only because the sellers were explicitly rejecting cash offers from investors. It was a family home, and they wanted it to go to someone who would maintain and live in it. Keep looking, keep trying, and maybe you'll get lucky too.

I dunno, I'm looking for a place to live, but ideally starting in July, so if I can get a better deal by offering the current owner/tenants free rent until then, that'd be perfect.

If you're starting a job in a new town in March, it's not a great option, but if you're looking months ahead of your preferred move date, why not?

Another why not-- you've just signed a tennancy lease. If they don't voluntarily leave on the assigned date, you need to run eviction proceedings.

where do you start? what grounds for evicition? Unpaid rent? You've already agreed that rent is zero...

Why would a REIT/Private Equity not care about this? Because their goal is to rent the property in any case. Professional landlords already have this in their risk models.

Trespass; at the expiration of the lease period, without an agreement (which can be inferred from acceptance of rent after the expiration, so don't do that) the tenants become trespassers.

> Unpaid rent?

That or other lease violations are typically only needed as the basis when the tenant has a current rental agreement. (Either in writing or inferred from acceptance of rent by the landlord.)

But, yes, the potential of having to deal with the process isn't something that should be ignored (nor are all the positive obligations on landlords.)

Why not pay thousands of dollars to let someone else live in your house for free? Is that a serious question?

The idea of rent-free occupancy wasn't even a thing two years ago. It's just sellers taking advantage of the current market where a lot of the buyers have no intention of living in the house and so a few months of rent-free occupancy make absolutely no difference as long as they get to buy the house.

No, for a house. If I'm spending $600,000-$700,000 on a house, paying $600,000 + three months rent is still on the lower end of that range. It's just a different structure, not more money.

Sure, but a month's rent is something like 0.5% of the cost of a house. If they simply offered 1.5% more for the house to get the one they wanted would anyone say "No person actually looking for a place to live would do that"?

$10k on the base offer or $10k in "free rent" is $10k either way.

The difference is that if they increased the price by $10K, you can get the loan to pay them, and you amortize that payment over 30 years. Many people are financially stressed enough to pay the downpayment - essentially you are saying the downpayment should go up by $10K. They may not have that $10K.

Yes, this is a very material difference to a lot of people, but the original claim was that it's something that only a speculator would do. I'm saying that as a person looking to buy and move into a house, this is 100% something I'd be happy to do.

Where I am, I'm seriously considering down payments in the hundreds of thousands. Should houses be that expensive? No, I personally believe we should build so much housing that it tanks the market. But the reality for people trying to buy a house here (Austin TX), +$10k to the down payment is insignificant compared to the price variation between home A and home B.

I wanted to highlight the alternative approach take by China. I don't agree with what their government, does but its useful to see what they're doing.

China has essentially realized they're in a demographic crisis so they've enacted the following policies:

- Stopped their speculative debt fueled housing bubble, this I hope makes it affordable for their citizens to own homes, without prices skyrocketing.

- Stopped for profit educational institutions, this is so that education and specifically tutoring aren't exclusively for the rich.

I think they're enacting policies for childcare as well.

Given in the US investors are buying up property, and costs of both education and childcare are skyrocketing. I don't see how the US won't avoid a demographics crisis as well.

The US can't mandate its industry to follow a similar approach, but can't the government provide stimulus or some other Manhattan Project type drive to encourage entrepreneurship and companies to start and resolve these underlying issues?

Why look to China when we can look to Japan? They had the worst housing bubble in world history, now housing is affordable. All thanks to a streamlined national zoning code that took power out of the hands of local government. There are twelve nuisance levels and you can build anything that falls below the maximum allowed nuisance level for a lot, no community approval process necessary.

Oh yes, I've seen videos about Japan's approachable housing. [1]. I'm sure Korea and other Asian nations have similar approaches.

I mainly wanted to highlight a market driven approach that works with the other industries in the US as opposed to a government directed one. Albeit the government provides stimulus of some type to kick start it, like how NASA drove the privatization of Space and now we have lots of launch vehicles via different companies.

Japan's population has also been flat since 1993. It's quite a different situation. Many countries have struggled to maintain sufficient new housing development to keep up with rising population numbers.

it appears that the US is heading in the other direction, with mandates to force developers build % affordable housing. Just let developers develop. Rich people move up, middle people move up, making the cheap places cheaper for low income residents. It's all backwards

China's alternative approach is hukou, which is in practice the only way US superstar cities could get what they want, to be both quaint and affordable: just ban people from moving there. China is allowing the countryside to urbanize but they are doing it at their own pace; it's not a free for all where every bright kid from every backwards place is simultaneously bidding up the price of housing in Beijing.

In the US these kinds of internal migration controls violate the Equal Protection clause, so they are mostly a pipe dream. Like anywhere, the US has a lot of places not worth living in, but the people from those places are all able to compete for spots in the cities, so those spots will necessarily be competitive.

So if that's the case, won't investing gov't funds into those uncompetitive places (e.g., by moving gov't agencies there, moving some industries that could move there etc) even out the level of competition?

Rather than spending money subsidizing the poor in these competitive places, it's better and cheaper imho, to add/create a good place to be in a currently bad place.

There might really be the magic window, where a place is big enough for real opportunities and amenities but small enough for cheap large-lot housing, high-mileage low-traffic commutes, and ample free parking. But if it exists, it's very narrow. We have no track record of getting population centers into that window or holding them there. Most population centers, whether driven by government spending or not, either undershoot or overshoot it in the end.

We have thousands upon thousands of towns sustained by the local military installation, prison, defense plant, research lab, state university, etc. Even some mid-sized metro areas where the economy is mostly Medicare. Usually it is more of a life support thing. They're too small to be desirable. On those occasions when they do take off and become desirable (defense spending made Silicon Valley!) they quickly become competitive.

Rather than trying to manufacture and maintain dozens of places on this knife's edge Goldilocks window for postwar sprawl (that may or may not exist), we could instead choose a building and transportation architecture that provides a high quality of life at reasonable cost over a wider range of population levels.

There's just too many folks here who'd rather make a quick buck then provide some longevity to the nation (at the top and in politics).

China and other nations realize that there is more money and happiness in the long term view, so they're either pivoting or have pivoted. I'm afraid we just don't have the gumption / community oriented view to do that here in the USA. Folks want "freedom", even if that freedom means degrading into massive poverty / wage slavery. I don't blame them particularly, our education system massively touts the successes of USA above all.

Seems like there has been pretty heavy asset inflation across the board for the past ~decade and investors are desperate for returns. I mean it seems to make sense, the ultra cheap money isn't really available to most people. Most people's marginal rate is probably a credit card at 20+%.

Big businesses/very wealthy can access very low rates by 1. pledging collateral and borrowing-> buy assets-> pushes asset prices up-> collateral worth more-> back to step 1.

With houses they know the average person(who is a homeowner) will fight tooth and nail to keep prices high. Especially people who have bought recently. The higher prices are the more incentive people have to keep them high as it becomes a greater % of their net worth. Tyranny of the majority.

Feels like in Canada we are basically seeing the emergence of some sort of neo-serfdom where the majority of young people(and older renters) who don't have significant family support are spending so much on rent they will never be able to own and year after year rent takes up a greater and greater amount of their salary. It's not at all uncommon to hear about people living in hallways or many people to a room in the GTA/GVA.

This is largely an artifact of low rates. Most retail thinks in terms of cash flow: what can I afford to buy (relative to rent) based on monthly cost. This includes mortgage (both principal and interest), insurance and taxes.

But investors, particularly institutions, think in terms of return on capital. The very important distinction is that the part of the mortgage payment going towards principal does not constitute a cost from a corporate accounting standpoint. Rather, principal payment goes on the balance sheet as accumulated equity in the property.

In other words retail is sensitive to total mortgage cost, whereas institutions are only sensitive to the interest component. As interest rates fall to zero, principal grows to nearly 100% of the mortgage payment. Even at todays rates principal constitutes about a third of the mortgage payment from day one, giving institutions nearly 50% more buying power. (Particularly in low property tax states like California.)

Besides raising rates, the only real option is to underwrite increasingly longer duration mortgages. When interest rates fall, extending the mortgage duration makes principal fall proportionately. Hence why many countries in the low rate macro environment have moved to 50 year mortgages to avoid systematically disadvantaging retail.

It's become basically impossible to buy a house as a normal person, even on a higher tech salary. In most markets around the US now, the expectation is that buyers will waive inspection requirements, make an offer as all-cash (e.g. pre-approved financing), with no contingencies (e.g. not based on sale of their previous home).

I'm currently trying to buy a different house, my older sister just bought a different farm, we both have had a horrible experience. My sister had multiple properties where her bid was beat out by someone offering $100k+ over ask, all-cash, mostly REITs and other types of corporate investors. This wasn't even in a city (farm obviously). I'm trying to find both a house and a place to rent, because my realtor/broker has advised me that I need to rent for at least a few months while I sell my existing house so I can buy with no contingencies, or I'll never get under contract. I finally found a proper spot for us to rent, was supposed to be available April 1st and was accepting leases starting March 15th according to the listing. Was just informed yesterday that the owner has already got it under application and has four other renters waiting in the wings.

This market is ridiculous if you actually need a place to live, and it's not even a matter of income. I'm in the top 1% of earners overall in the US, and I can't even close the deal on a place to live. I've had my current house for a bit over ten years, and it makes me almost want to give up and not move, although I must for family reasons. When I look into it, most of the properties being swept under me (and others) aren't even being bought by people, they're being bought by REITs or other investment vehicles, mostly by foreign money. You've also got companies like OpenDoor and Zillow scooping even high-earners trying to buy a place to live.

> It's become basically impossible to buy a house as a normal person, even on a higher tech salary. In most markets around the US now, the expectation is that buyers will waive inspection requirements, make an offer as all-cash (e.g. pre-approved financing), with no contingencies (e.g. not based on sale of their previous home).

In some places that may be true, but I was able to get a home last January on a single relatively moderate-high tech salary, I have a friend that signed for a home on a single person decent salary as well near me, and my next door neighbors again single relatively decent tech salary just bought a new home elsewhere.

You may be right about places in like LA or Toronto or NYC, but to generalize that everywhere is a little absurd. I know that the market I fled in UT was that way, and things are getting pricier here in the neighborhood that I am living in, but we are definitely in the middle of a crazy bubble right now; however it won't last forever, things are going to pop eventually. There are good affordable places to live even if they aren't in CA. Much of the Midwest is great, I think part of the bump we are seeing is rise of remote work exacerbated an already existing bubble brought about by government subsidization as it allowed tech salaries to be redistributed geographically.

I do agree that part of the problem is large investment firms purchasing housing as an investment and an article the other day on here pointed out how they are able to take advantage of government subsidies to purchase more homes, but a bubble can't last forever it will pop, and I feel like the popping is going to come soon.

It's just more anecdata but I live in Western MA and this is exactly the situation we have out here: people are being pressured to waive inspection and to offer in cash and without contingencies. Honestly, it seems crazy risky to me to buy a home under those terms and I suspect that regular people simply end up renting.

> This market is ridiculous if you actually need a place to live, and it's not even a matter of income.

The US needs to make a policy decision: are houses investments or a way to nurture and grow the lower and middle class?

If it's the former, they can use tax policies to encourage the desired behavior. Tax every residential home (single family or condominium) at 10-30% of its total value per year, regardless of who owns it. Give a complete write off for your first home. Maybe give a partial write off for your second home. Make owners bear the cost of appraisals, and if appraisals aren't available, tax them at the most expensive 90th percentile.

But of course maybe the US decides homes are investments. Great for the wealthy, but the lower and middle classes are really going to get hurt. Birth rates will slip even further.

> The US needs to make a policy decision: are houses investments or a way to nurture and grow the lower and middle class?

They already have. home buyer loans are backed by the government. You can write off loan interest. Investors pay taxes on income from the investment (net rent and capital gains) ...

Also just like in education space the more the government subsidizes the pricing, the more it gets inflated. So more incentives will just lead to more demand and higher prices.

What we really need is more supply and elasticity. More houses, and more people willing to say "F--- this I'm moving to CheapTown"

> just like in education space the more the government subsidizes the pricing, the more it gets inflated.

People keep saying this, but I haven't seen any real evidence of that. In education or personal home ownership. Do you have any studies that actually show any causation, or is this all correlation?

> But of course maybe the US decides homes are investments

They have. By not deciding, they have decided. It would be incredibly harmful to reverse course now. Typical US policy is to get backed into a corner until doing the right & obvious thing is incredibly difficult and practically impossible.

They're also welcome to change this decision at any time if enough of the electorate demands it, or if it becomes obvious it will lead to impacts to the policy stakeholders.

I found your comment thoughtful, but it seems to me you meant “latter” rather than “former”? iirc hacker news let’s you edit a comment for up to an hour after posting.

Wouldn't that tax proposal just increase rent for people who don't own their home (landlords pass on the costs) and not affect homeowners other than lowering the value of their home if they come to sell it (i.e. upside-down on mortgage).

Well they made an exception for the first building. In general if you construct laws such that the property tax is progressive on total assets then there is a pricing advantage for smaller landlords. They can charge lower rates, make more profit, etc.

Do you actually have any evidence this is true in "most" markets? It seems like only in a few markets around highly-desirable cities is this true. Farms don't sound like they're going to be representative of the types of housing that most people are looking for.

I'm 45 minutes south of Seattle and I purchased a large house with a backyard, recent-ish construction, no contingencies waived, for less than what a 500sqft loft is going for in Seattle.

Farms are also what investors are looking for, at least the types of farms this person seems to be talking about. "Farm" the land for 10-20 years, and then put in a development as the city grows out. These investors are betting that the land will be worth a lot more in a few years.

I put farm in quotes because they are intentionally mining the land of all long term fertility - not a problem as it won't be farmed in a few years anyway, but if you intended to farm for more than 10 years then proper care for the land will ensure better profits of the wrong run.

This explains why a half assed, poorly maintained, corn crop would randomly pop up in a lot between commercial buildings, across from where I used to live.

I live in a rural area (relatively speaking - town of about 1000 people) - around me if you don't show up to look at a house, ready to buy, and with no contingencies - you are not going to get a house. I know many folks near me who have listed their house, had 40 people show up the first day (open house) and sold it the next day, for cash, for 20% over the asking price - around me, those stories are very common.

I study the RE market in several places that I am connected to every day - I watch houses come on the market, and are under deposit within days. I feel really bad for young people looking to buy their first place (including my kids) - they can't pay cash, and they are on a budget - they have almost zero real options other than to continue to rent and wait for a RE crash. IMO, it's coming, but who knows when.

Home prices around where I am (LCOL area in MI) are creeping up, but not to the absurd degree they are in actually desirable places to live. That said, anywhere that's decent to live is getting slammed. For instance, sticking to MI, Grand Rapids and the Ann Arbor area are insane compared to where they were a few years ago.

The only reason there are any decently priced houses where I am is that a lot of them are over 100 years old and some of the school systems are so bad even our current asset bubble can't make families want to live there. (So no point in buying to rent out for twice the mortgage because no family is paying 2000/mo for a house in a school district with a math proficiency rate of 15%.)

It's also creating a situation where the actual quality/value of properties for price is completely out of whack. There are large swaths of the country where low-grade cookie cutter houses in the suburbs that are legitimately worth maybe $350k at the current inflation rate are asking for $850k+ and generally selling $100k+ over ask. I have a $1.25M budget for a house and I can't find anything that's not a trash heap I can afford, and I'm not even looking in a coastal area, this isn't the legendary market in California, this is in the middle of the US.

It astounds me that more homes weren't wiped out from the Northridge earthquake. A lot of the housing stock in California in particular is like rotting toothpicks on eroding sand for a foundation. At least the homes generally lack basements so they will only fall a few feet off the posts. This particular reddit users is a contractor that posts their typical finds from structural inspections. People are paying between 800k-5m for the homes featured, generally:

Where you see winters homes are generally even in worse shape. Basements are leaking and eroding your foundation. Roofs are leaking and rotting your studs. Poor insulation is costing you a lot more money than in California. Chances are your water mains and sewer situation, both from your parcel as well as the municipal lines on the street, are all approaching end of life. Right as climate change brings heavier rains and flooding that stresses infrastructure where there isn't money as it is to maintain it even for old climate projections.

It's a real concern of mine and it's driving me towards considering building a custom home, at this point it's almost cheaper to do, especially since much of the work I can do myself and already have the necessary skills and tools. It's really and truly absurd what people are being expected to pay in comparison to what they get... I feel like most of the houses in the US are actually unsafe to live in because they don't care in construction about efficiency, indoor air quality, or mitigating common environmental concerns in those areas like radon gas. The minimal building codes in the US are truly obscene, and yet these slapdash houses are now priced for 3-4x what they are actually "worth" given the inflation rate.

I have a 5 page document of bullet points making simple asks/requirements for a new home build, and most of them are focused on safety, reliability, and efficiency, and none of them would be done by default by any builder in the US, most are required by law in Europe. It's kind of nuts.

Sure, this is non-exhaustive of course, but here's a few of the items on the list I personally think are very important.

* Foundation footings set to bedrock and insulated above the freeze line

* Exterior walls framed in 2x6 or 2x8 studs w/ a preference for non-bridging stud products like t-studs

* Exterior continuous insulation

* Kitchen range hood needs to be externally ventilated with proper make-up air system

* Using an ERV (Energy Recovery Ventilator) with filtered intakes for doing fresh air distribution within the home

* No use of plastic flooring products (e.g. linoleum, vinyl, carpet, LVP, LVT, et al) which off-gas and spread plasticizers within the indoor envelope

* Consider use of alternative methods of framing vs stick framing, like using ICF (Insulated Concrete Forms)

* Natural gas on-demand hot water heaters w/ electric instant hot systems close to tap for showers

* Roof trusses and decking properly constructed to account for the weight of solar panels on the south-facing slope

* Split electrical paneling for high voltage (230V+) and low voltage (120V) circuits

* Post-meter paneling for breaking out to circuit panels w/ a space for setting up a transfer switch to support future grid-tied solar with battery backup

* All electric appliances w/ the exception of on-demand water heater and sealed gas fireplace, this provides a pathway for higher energy efficiency / lower carbon emissions by using solar

* All cabinet work should be hung using french cleats for durability

* Exterior door frames should be installed fully to the studs (e.g. use 3-4" long screws)

* Interior doors should be solid core

* All interior walls should contain sound-rated insulation to reduce noise pollution and improve climate zoning

* All interior walls should be boarded with sound-sealant and noise rated drywall-type products

* Subfloors should be insulated and there should be sound/thermal insulation underlayment below the flooring

* The final construction prior to drywall should be able to achieve a blower door test score of ACH50 1.5 or lower with the make-up air and flue vents closed.

Not all of these things would be required by code currently in Europe, but they're all good ideas for durability, efficiency, or safety. This is obviously with the intent to use rooftop solar power as well. If I do build a custom house, it'll be built to the Passivhaus standard.

Your list is a 100% match with my requirements list for my build in the Chicago area in 2018. Sounds like you may have also spent a lot of time on Green Building Advisor articles and forums.

Our biggest challenge was finding contractors willing to execute to plan. My wife and I ended up doing a lot of work ourselves especially around insulation details and HVAC systems.

Yes, I am a big fan of Green Building Advisor and I also watch a lot of building YouTubers, predominantly Matt Risinger's Build Show[1].

He has featured other builders and home owners who also have websites or channels, and there I've found more information. There was one chap in central Canada that built a ~5k sqft house that only needed around 1600W to heat in the winter in subzero temperatures. That's the type of energy efficiency we need in new home construction if we're ever going to make a dent in climate change.

> Foundation footings set to bedrock and insulated above the freeze line

Not knocking it, but is this normal for single family home construction? Is it possible with reasonable cost? Is it primarily for an earthquake-prone region? The idea is cool, but I thought only skyscrapers went down to bedrock.

The answers to your questions definitely vary by region. If you're building a house, one of the first things you should do is get a structural engineer's assessment of the lot before you plan the foundation, because soil type, bedrock depth, freeze lines, environmental concerns, etc. all affect this.

But yes, it's fairly common to do this if you care about structural integrity over the long term. In areas with soil type that support it, it's more common to do simple slab foundations without footings, but in most of the US footings are used and the foundation is built as part of a crawl space or basement. Sometimes excavation for a basement is deep enough to get below frost line, or to bedrock itself, it depends greatly on the region.

"Reasonable cost" is kind of a subjective thing, but I'd say starting with a a good foundation is a bare minimum of requirements for what would end up qualifying as "constructed properly", so at least as far as I'm concerned this is an absolute requirement.

I'm still confused. Basements go below frost line, sure, but bedrock can be hundreds of feet below the surface. I don't know of any home I've ever seen that has piles driven down to bedrock. Is this just a regional thing? What am I missing here?

Yes, bedrock can be many hundreds of feet below the surface, and in other areas bedrock can be pretty near to the surface. This is one reason why you should have a geologic and structural engineering report done on a plot before you build (and arguably before you buy the plot). Depth to bedrock greatly factors into the cost if you intend to have piles put in to support your foundation.